Mankiw’s Principles of Economics Part 9: Prices Rise When the Government Prints Too Much Money

The introduction to this series is here.

Part 1 is here.

Part 2 is here.

Part 3 is here.

Part 4 is here.

Part 5 is here.

Part 6 is here.

Part 7 is here.

Part 8 is here.

Mankiw’s ninth principle of economics is: Prices Rise When the Government Prints Too Much Money. He describes hyperinflation in the Weimar Republic in Germany in the early 1920s. The US hasn’t experienced hyperinflation, but it has had problems with inflation, as in the 1970s. He says that inflation imposes costs on societies, so a goal of policymakers is to keep it under control. He tells us the cause of inflation:

In almost all cases of large or persistent inflation, the culprit is growth in the quantity of money. When a government creates large quantities of the nation’s money, the value of the money falls. … The high inflation of the 1970s was associated with rapid growth in the quantity of money, and the low inflation of more recent experience was associated with slow growth in the quantity of money.

As stated, this principle doesn’t sound quite right. In the US, at least, the government doesn’t print money, as we found out in the uproar over the Trillion Dollar Coin. That idea brought out the flying monkeys, shrieking that it would be wildly illegal for the Treasury to mint money other than small coins. According to Mankiw, in the US substantially all money is created by banks, as he explains in Chapters 16 and 17. He gives the standard description of fractional reserve banking. He explains that the Federal Reserve Board can add to bank reserves, thus creating the possibility of new loans that will create new money, or reduce reserves, reducing the ability of banks to create new money. These tools enable the Fed to control the money supply. He acknowledges that there are serious difficulties facing the Fed in exercising that control, but he claims it can be done as long as the Fed is “vigilant”. Chapter 16, page 339. With this explanation, it is not clear why Mankiw claims that government is responsible for inflation by printing too much money.

One of the difficulties Mankiw describes is the problem of measuring the money supply. In the US, there are two broad measures of the money supply, M1 and M2. The Fed quit publishing a third figure, M3, in 2006, but it is estimated by the OECD. Here’s a handy chart from Wikipedia showing the various measurements of money supply. For those interested, here’s an Austrian definition of money supply. And here’s an argument for including repurchase agreements in the calculation of the money supply. I’m not quite sure how Mankiw would measure the money supply for his principle, especially because other economists don’t agree.

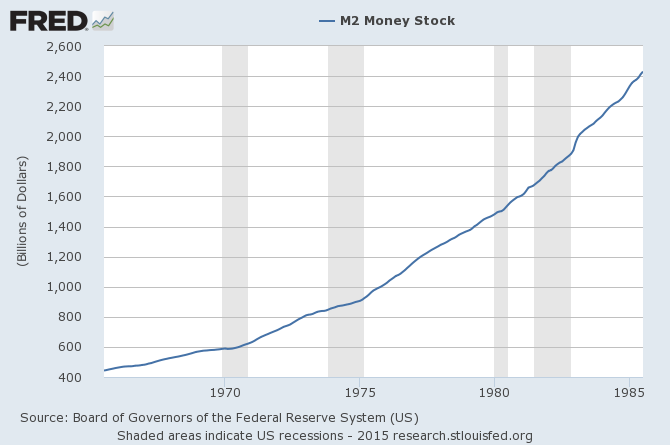

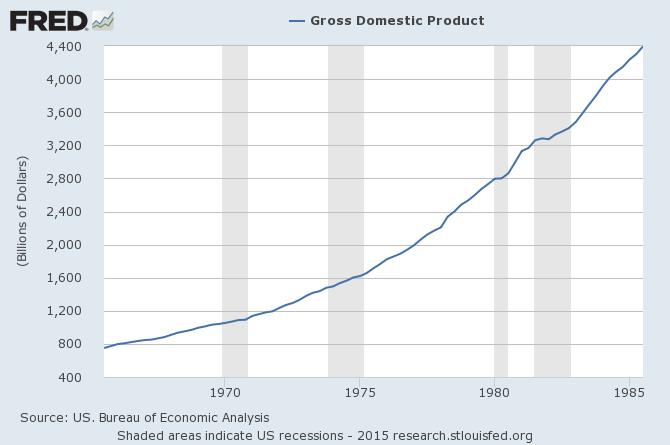

I’m also not sure what to make of Mankiw’s claim that the inflation of the 1970s was associated with a “rapid increase in the quantity of money.” Here’s a chart showing the growth of M2 for the period 1965 through 1985. It looks like it is rising, a bit faster after each recession (grey bars). It looks to me like the next chart, gross domestic product over the same period seasonally adjusted. Perhaps there is some other factor, or maybe I’m just reading this wrong.

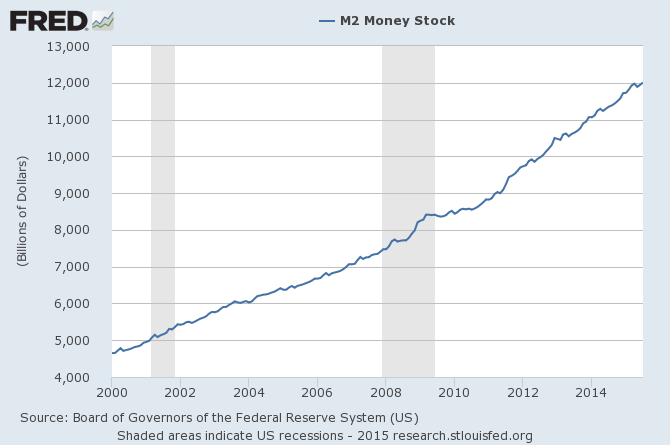

Here’s a chart of M2 from 2000 to the present. There is a noticeable increase in the rate of growth of the money supply in the immediate wake of the Great Crash, leveling off in March 2009. Starting about August 2010, the increase is again greater than in the pre-Crash years. These rapid increases in the money supply match up with the Fed’s Quantitative Easing programs. It has not, as many economists (not Mankiw) predicted, led to rapid inflation.

That points us to the central question raised by the principle: how much money is too much? If Principle 9 were a scientific principle, we could use it to work out an equation for the correct amount of money, either empirically or theoretically. Mankiw doesn’t offer either. Instead, he has a section explaining the debate between those who think the Fed should have discretion and those who think the Fed should follow a strict rule, like increasing the money supply by 3% per annum. P. 520. It isn’t much of a principle if it doesn’t lead anywhere, and doesn’t predict anything.

Mankiw’s phrasing, blaming the government for inflation because of its intervention with the operation of markets, fits nicely with Mirowski’s 10th Commandment: Thou Shalt Not Blame Corporations and Monopolies. It supports Mirowski’s Third Commandment, calling for full reliance on the marvelous market and making sure governments don’t interfere. We get a good look at this in a recent paper by Thomas Palley who has been writing about neoliberalism for some time, titled The US Economy: Explaining Stagnation and Why It Will Persist. Palley says that there are three explanations for the Great Crash.

1. The hardcore neoliberal explanation: it was all the fault of the government. Interest rates were forced too low for too long in the wake of the 2000 recession, interfering with the market for money. For purely political reasons, the government intervened in the housing market to encourage increased homeownership, leading to misallocation of scarce financial and other resources. This is the position of Peter Wallison of the AEI, whose dissent from the Final Report of the Financial Crisis Inquiry Commission explains this view. It is not recommended reading.

2. The softcore neoliberal explanation: it was the fault of government regulators. The regulators allowed excessive risk-taking by lenders, and perverse incentive pay structures in the financial sector. They allowed deregulation to proceed too far. That enabled bad allocation of the flood of foreign savings into an overblown housing sector. When it popped, the resulting financial disorder deepened a structural business cycle recession into a near depression.

3. The Keynesian explanation: neoliberalism did us in. The explanation is that neoliberal policies destroyed the institutions and rules that kept corporate greed in check and made sure that the benefits of a growing economy were shared between capital and labor. In the end, consumer demand was crushed by inadequate wages. It slowed to the point that it could not drive economic growth as it had during the period 1950-75. As incomes dropped, debt rose, so that when the Great Recession hit, there was no demand left to drive a recovery. The cycle of jobless recoveries has come to the point that stagnation is the plausible future for the US economy.

Mankiw argues for neoliberal explanations and solutions and certainly not the Keynesian explanation or its solutions. For example, in October 2008, he wrote that the Great Depression was largely cured by monetary policy, and pointed to studies saying that New Deal legislation like the expansion of labor rights was counter-productive because it allowed labor power to interfere with market forces.

I don’t doubt that the quantity of money might have something to do with inflation in some cases. I’m not convinced that it explains either the inflation of the 1970s, the lack of inflation in recent times, or the current inflation in Russia.

This one comes back to the question of what is money. Prior to the Crash, the hedging credit default swaps were creating transnational money such that when the crash came no one knew how much of that notional $100 trillion was actually at risk. Real taxpayers’ money had then to buck up the “confidence” of those at risk and the Fed had to prop up insolvent US banks against their counterparties to prevent more of that notional $100 trilion from becoming real. It was seven levels of fraud in the banking system that created that risk from $100 trillion of notional money and the hedge funds and credit default swaps that monetized (armed) that risk.

It was the international financial industry itself that printed too much money and made sure that only they could benefit from its existence. And it was all levels of government that stuck the losses on homeowners and workers through failure to prosecute and international austerity policies.

Prices actually fell because the crash took several trillion dollars out of the global economy. And the cost-cutting reaction took more.

Prices rise when the amount of money is sufficient more than the available supply of goods and services in the right pattern of demand that individual buyers can bid up the price in order to ensure that they get the good or service. Or at least that’s the way it used to be explained under the hydraulic model of the economy. The government need not be involved in that disequilibrium. It is sufficient that foreign oil supplies be manipulated political by foreign governments in a time in which the government has anxieties about war debt that it deferred for a decade and during a buildup in military spending and private anxiety about rising wages. Not to mention that at that time, recycling all the petrodollars the oil-producing nations were taking in caused distortions in prices for individual assets, such as commodities or real estate (especially agricultural real estate).

I agree. Remember the $147 a barrel oil? Today oil closed near $40. Somebody made a lot on that. I bet Bush, Cheney and the Kochs made out big time. And then the MIC made a bundle on Iraq and they still are. They now have their sights on Iran. But this time it could be a bridge too far, I hope.

.

The fraud around the housing bubble was biblical. And no one seemed to care and no one went to jail and the same banks are out there fixing the London interbank rate and prices of derivatives. One could almost think we are headed there again.

.

Meanwhlle, Joe Sixpack makes $7 to $10 an hour and needs food stamps to survive and is called a loser and taker by his “betters”. Even $17 an hour won’t help since now you have this wonderful thing called the ACA which will bankrupt your losing ass, if you get sick or even if you have a complication in child delivery. But hell no, we can’t have abortion for ten year olds who are raped. Our enemy, I bet, are the undocumented murders and rapists that Mexico sends us. Well them or the Muslims. One of them.

What I would like to know… where IS all this money the USG has been printing for the last 50 years? I’d submit it’s in offshore Corporate and 1% accounts. It would be enlightening to see how much money is in Corporate and 1%(I repeat myself) today. Vs,… money in circulation for the 99%. If it were really known, guillotines couldn’t be built fast enough.

This is a really interesting question. Take a look at this graph: https://research.stlouisfed.org/fred2/graph/?s%5B1%5D%5Bid%5D=AMBNS

It shows that between mid-2010 and the present, the reserves of banks at the Fed have risen by about $3.2 Trillion. That isn’t going into the economy, but it bolsters the bank’s balance sheets. The Fed pays a small amount of interest on those reserves,.25% as discussed here: http://seekingalpha.com/article/3015696-the-interest-rate-on-excess-reserves-is-the-new-fed-funds-rate

This may explain why the money more or less created by the Fed and the Treasury in these transactions didn’t lead to inflation, according to this: http://www.economicshelp.org/blog/111/inflation/money-supply-inflation/ He argues that the banks didn’t lend money so it didn’t go into the economy, and thus could not ever lead to inflation. This is the pushing on a rope argument more or less made by Mankiw, who says that the Fed could create the conditions for increased loans by increasing bank reserves. Of course, the Fed can’t make banks lend, any more than it can in the short term bar banks from making stupid or fraudulent loans.

Wow! Just wow! Where to begin. First, of course inflation can be caused by printing too money if you spend it. Like if you give a basketful of hundred dollar bills to every citizen, you may get your wish. But note that unless you keep it up, there is likely to be only a one time inflation or increase in the price level followed perhaps by a deflation.

.

I love it when folks talk about the Weimar republic and conveniently neglect to say the French and Belgium’s invaded the Ruhr and took over their manufacturing when the Germans could not make a payment and then a strike ensued and the Germans lost much of their productive capacity or that the German reparations were in a foreign currency or gold and Germany was thereby forced to buy it on the market when no one wanted marks. So they printed money but not just one time, repeatedly, so that something like 14 trillion were needed for one dollar. Or that it was ultimately resolved. Funny that.

.

Then there is our 70s inflation. Money caused it? How about the Saudis and the price of oil. It was a supply shock. And, of course, Volcker came along and raised interest rates to 20%. Brilliant, our neoliberal friends would say. By then the inflation had adjusted to the new prices from OPEC. But let’s be clear about that. Who benefits from very high interest rates? Guesses anyone. Now we may face food shortages and increased prices. Speculators are already betting on it. Money can’t solve supply shortages or worldwide famine from climate changes.

.

The softcore neoliberal explanation is in the ball park. The other two not so much, including the so called Keynesian one. The great recession was a result of a financial bubble generated by fraud that ended in insolvency and massive layoffs. In my view (not held by many on the left) is that if the Fed had not bailed out the financial institutions, the insolvency would have triggered a depression somewhat worse or much worse than we saw. The really fucked up mess was the several thousand pages of Dodd Frank, much of which will never be implemented. No one could see their way clear to reinstate Glass Steagall. And we missed the chance to break the gambling banks up or to jail a few of them to teach them what moral hazard is all about.

.

One other note. Inflation can occur when demand exceeds capacity (read employment for the most part), not necessarily when someone prints money. And lets be clear here. Banks do not create new net financial assets. There is an offsetting debit and credit for every loan. And they loan based on their view of profits, not reserves and often go off the rails into gambling and insolvency. Only the government can create new net financial assets as a byproduct of a deficit.

If banks had made loans with all those increased reserves provided by Fed actions, we might have seen more economic activity, and we might even have seen some inflation. That doesn’t seem to have happened, per my previous comment. I’ve argued at length in posts at FDL that the banks wouldn’t lend if there were no demand for loans. Increasing reserves is just pushing on a rope.

*

Your point on the causes of Weimar hyperinflation is well-taken. Yves Smith has a couple of posts on this, here’s one: http://www.nakedcapitalism.com/2010/03/parenteau-the-hyperinflation-hyperventalists.html I certainly agree that Mankiw is too facile in this brief discussion. There is a bit more later, starting around page 392 (in the 6th edition), but it’s pretty simple. The more complex discussions at Naked Capitalism are much more helpful.

Mr. Mankiw seems not to remember defense spending as a major cause of 1970’s inflation. Examples: Paying for the Vietnam war. Maintaining large armies in Germany, Korea, Japan. Cold war spending on arms, military “aid” and training. Supporting rightwing governments and opposition parties in places such as Chile, Italy, the UK, Indonesia, the Philippines, Australia, Latin America. And increasingly bizarre black box projects, such as having an opaquely-controlled Hughes organization build a custom ship to recover a sunken Russian nuclear submarine. That’s a lot of money, much of it spent, rerouted to or invested in the United States. That’s not “intervention” in the market. That’s government as a precondition for and significant part of the market.

Two feet good, four feet bad. Mr. Mankiw seems to contend that government and labor can only interfere with markets, not participate in them. That would leave corporations as the only legitimate market participants. That is, until they need contracts and copyrights enforced; labor muzzled; and foreign and international laws supplanted by secret business-dominated conventions.

I only know about this guy from what Ed posts here. Some of Mankiw’s stuff seems rational and superficially correct. But a layer or two down it falls apart to me, a non economist to be sure. So the wonderment: is he just plain stupid or pimping for his masters? He has a PhD. the pimp.

He is a Harvard professor, former advisor to George W., and the author, I believe, of the most popular current economics textbook. He’s also famous for his students walking out of his class back in 2011 in order to join an Occupy march. The students’ protest letter doesn’t say much for the intellectual abilities of Harvard economics students as they clearly bought into Mankiw’s version of Adam Smith lock, stock and barrel. No doubt they’ve all since graduated and many now have jobs working in financial services.

*

The rise of large corporations, the failure to regulate them, and corruption are nothing new. Mankiw ignores the fact that Smith explicitly cites the need for a “well-governed society”. So much for government interference in the market. There is no market without government. The issue is what type of government: one that channels self-interest in the service of the public interest or one captured by private interests to serve private interests? Wealth of Nations is a critique of an economic system of the latter type and an argument for the former.

*

Related to the issue of corporations and their relationship to government, here’s a link to another paper that compliments the Meeropol paper I linked to back in the responses to Ed’s Principle 7 post: Sankar Muthu’s Adam Smith’s Critique of International Trading Companies: Theorizing “Globalization” in the Age of Enlightenment. The notes have many pointers to recent works in the history of economics that run counter to the nonsense peddled in economics departments, the media and in popular political discourse.

You have obviously read a good deal of Adam Smith. I once read portions of his “Wealth of Nations” but I doubt I understood much of it. It does seem though that lots of these so called brilliant economists misquote him a good deal. I continue to believe none could be so stupid. So the only explanation I have for them is they are pimping for the powers that be. On another note, I have long since lost my esteem for Harvard training. It doesn’t impress me much.

Well, exactly. You don’t have to read a lot of Adam Smith to figure out that they are selectively quoting. Just look up their quotes and read the context. (One wonders why those Harvard students had to have Mankiw tell them what Adam Smith argued or felt they needed his permission to consult primary sources–were they too cowed and lazy to take a trip to Widener library?) The more you read, the more you realize ‘Adam Smith’ is just a token that confers legitimacy to neoclassical economics; Smith’s arguments are irrelevant. ‘Smith’ is the tribe’s origin myth, their idol. Are economists illiterate, or loathed to read primary sources, or are they knowing and calculated, or is it just that some dubious but convenient claim has been repeated so many times that it has become a fact? “What, you doubt the invisible hand?!”

*

Foucault writes in his essay Nietzsche, Genealogy, History:

A decent explanation of money, currency, income, legal and accounting fictions, economics, finance, and a universal basic income via a new private, debt-free, digital currency (based upon principles of MMT, Monetary Sovereignty, and Lincoln’s Greenbacks) can be found here: “http://www.i-globals.org” aka the WGO. On its “Critics” page, “money printing” is a last resort of failed governments without sufficient assets to pay debts denominated in currencies they do not have and cannot create. Best wishes to this fine blog and the excellent commentators.

Maybe what matters (in addition to other factors) where the extra money is put. Neoliberalism always threaten inflation if money is given to those in the bottom of the economy because (naturally) corporations will adjust to these increased costs by raising prices and then passing that back onto the consumer, thus re-establishing more or less the previous relative inequalities. (I would argue that each level above those who received such largesse also clamoring for their salaries to be increased plays a role as well.).

But if all the extra money is given to those at the top, a different dynamic occurs: inflation, but in the luxury market. Therefore we see the prices of luxury items (condos in NY and London, art, etc.) rising astronomically. Unlike the automatic “trickle-up” that occurs when wages of workers are raised, there is trickle-down from the wealthy only to the extent that the items they buy actually involve more production and therefore jobs – which is not the case for existing apartments or fine art.

I think this has a lot to do with it. Banks aren’t lending for working capital for new businesses or even much to buy capital equipment, because there isn’t much of that, and because margins are low. I imagine they are lending to the rich, though, to finance the purchase by one rich person from another. The seller uses the money to pay off loans, and the money never hits the economy where we peons live.