The Slow Death of Neoliberalism: Part 2

The Slow Death of Neoliberalism Part 1.

This post focuses on the failings of neoliberal economic theory. Neoliberalism arises out of positivist philosophy, defined in Part 1. Positivism is the theory that the only true knowledge comes from the scientific process.

There are five main principles behind Positivism:

1. The logic of inquiry is the same across all sciences (both social and natural).

2. The goal of inquiry is to explain and predict, and thereby to discover necessary and sufficient conditions for any phenomenon.

3. Research should be empirically observable with human senses, and should use inductive logic to develop statements that can be tested.

4. Science is not the same as common sense, and researchers must be careful not to let common sense bias their research.

5. Science should be judged by logic, and should be as value-free as possible. The ultimate goal of science is to produce knowledge, regardless of politics, morals, values, etc.

Economists created a group of sayings which they put in their introductory textbooks and teach as laws and principles to their students at all levels. For example, N. Gregory Mankiw, economics professor at Harvard, starts his introductory economics textbook Principles of Macroeconomics with a list of ten Principles he claims almost all economists agree are true. Any thoughtful person reading this list will see that these ten statements are either tautological (you can’t do two things at once) or are mere rules of thumb. The idea that you could build a positivist science on this foundation is absurd. But Mankiw disagrees, and so does everyone who took Econ 101 and stopped, and especially so do the elites from our top schools.

It’s not surprising, then, that this version of economics is failing. It cannot perform the basic goal of a scientific theory, making accurate predictions. Economic models have failed and will continue to fail to predict disasters; and there isn’t much hope that they will ever be able to predict anything of interest.

In Part 1 I pointed out that the positivist program can’t be easily adapted to the social sciences. David Andolfatto of the St. Louis Fed agrees, and tells us what we can expect from economics:

But seriously, the delivery of precise time-dated forecasts of events is a mug’s game. If this is your goal, then you probably can’t beat theory-free statistical forecasting techniques. But this is not what economics is about. The goal, instead, is to develop theories that can be used to organize our thinking about various aspects of the way an economy functions. Most of these theories are “partial” in nature, designed to address a specific set of phenomena (there is no “grand unifying theory” so many theories coexist). These theories can also be used to make conditional forecasts: IF a set of circumstances hold, THEN a number of events are likely to follow. The models based on these theories can be used as laboratories to test and measure the effect, and desirability, of alternative hypothetical policy interventions (something not possible with purely statistical forecasting models).

This obvious straw man at the beginning of this quote is typical of the arrogant economist described by Marion Fourcade. But let’s see how well the economist business does at the weak test of effectiveness offered by Andolfatto.

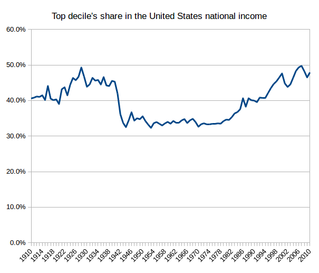

For decades economists taught the Kuznets Curve which they said shows that as industrialization proceeds, economic inequality first rises and then falls.

Thomas Piketty takes up this theory in Capital In The Twenty-First Century, and extends the data forwards and backwards from the early 1950s. Here’s a graph of top decile income share from 1910 to 2010 from Wikipedia.

Looking at that graph through the time Kuznets wrote, the early 50s, it might be read to support that hypothesis. The sudden rise, starting under Reagan and continuing ever since, completely contradicts the hypothesis. That didn’t stop people from teaching it.

The Phillips Curve asserts that there is a connection between inflation and unemployment: as the unemployment rate drops, inflation increases. It’s one of Mankiw’s 10 principles; and it’s deeply embedded in the models used by the Fed to decide interest rates. It’s mostly wrong. Here’s a recent debunking from the Philadelphia Fed, concluding that the Phillips Curve might help forecast inflation in a weak economy, but does not work in an expanding economy.

The Wikipedia Page for Phillips Curve says that:

The original Phillips curve literature was not based on the unaided application of economic theory. Instead, it was based on empirical generalizations. After that, economists tried to develop theories that fit the data.

A 2008 paper, The History of the Phillips Curve: Consensus and Bifurcation, Economica (2008), P. 10, lays out the history in detail. Roughly speaking, it begins with the observation by William Phillips that in the UK there was a stable relation between the rate of wage growth and inflation over a substantial period of time, and deviations could be explained reasonably. This paper was picked up by Paul Samuelson and Robert Solow and turned into the earliest mathematical formula in 1958. Since then there have been a number of occasions where the Phillips Curve failed, and each time economists just grab some more of their existing tools and try to fix it or explain the failure, in each case after policy-makers have gone on as if it were right and forced bad results on the economy and especially the wages of workers.

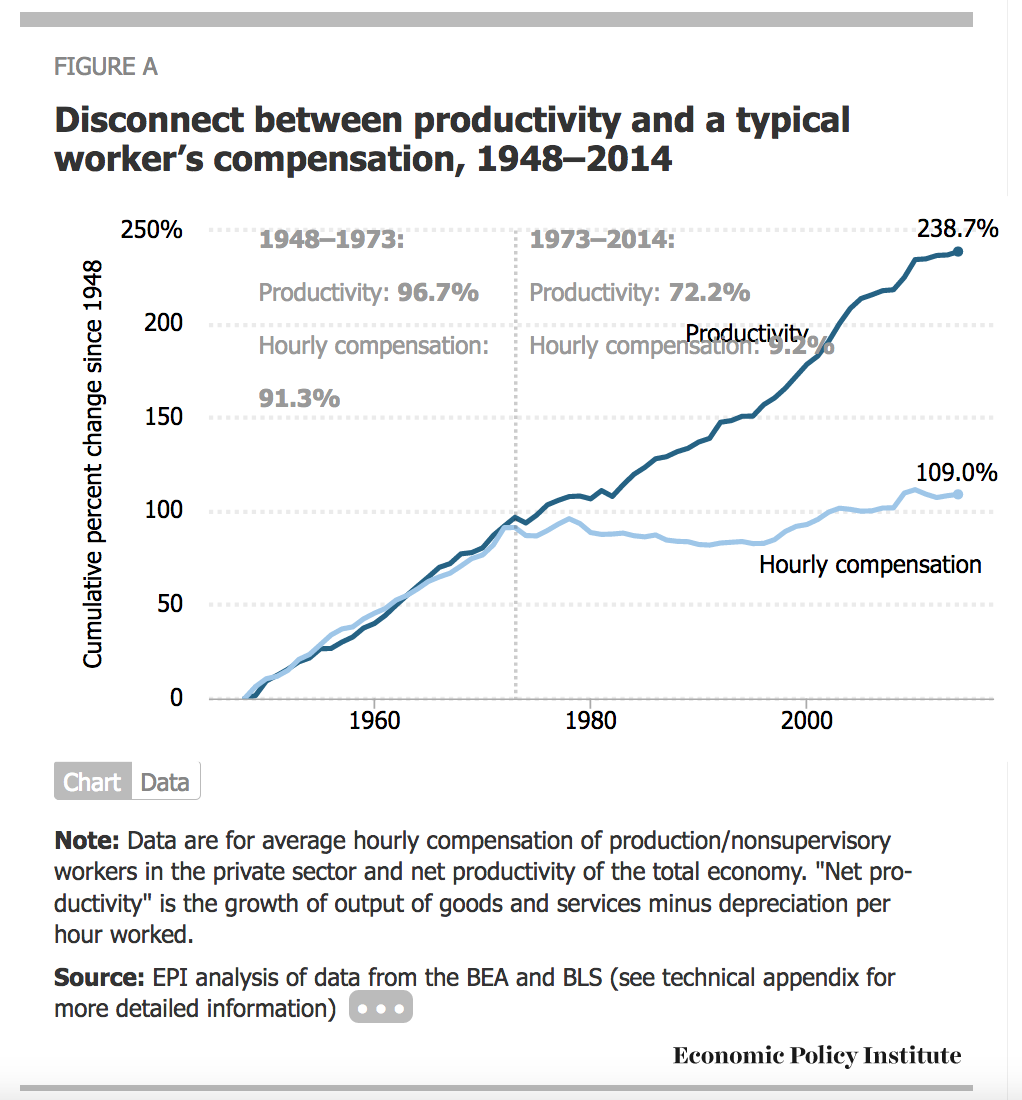

Here’s a third example. Economists say that the reason wages are stagnant is that productivity is flat, as if there were a relation between wages and productivity. Anyone who looks at this chart and reads this article from the Economic Policy Institute will have a huge question about that.

And that isn’t just the right-wing. Plenty of centrist Democrats make the same argument. And by the way, what does this say about the central theory of free market economics that supply and demand for labor set prices?

As I say here and here, neoliberal economists used their ideology of free markets to influence policy and to change the entire way we think about society without having the slightest idea of the consequences of their meddling because their models aren’t designed to deal with changes in societies or economies. As my examples show, they just keep on regardless of the success or failure of their predictions, and politicians and rich people ignore the failings and continue to follow their foolish advice.

Neoliberal economics obviously fails to measure up to the standards of positivism. It can’t predict anything useful, and it barely is able to explain itself coherently. That’s a problem with positivism too. People are slowly, slowly coming to grips with these failures and the damage they have done. It’s adherents are dying off, and their replacements are into it for the money and the power. Stupid ideas never die, but maybe they will lose their influence.

Updated to correct link to EPI article and chart.