Testing The Limits on Wealth Inequality

In this post, I pointed out that we are going to see an empirical test of Piketty’s theory of rising wealth inequality. The theory itself is not well understood, and Piketty has revisited it since the publication of Capital in the Twenty-First Century, and published an economist’s dream of a paper in full mathematical glory here. The American Economics Association devoted space in its journal to arguments about the theory, giving Piketty an opportunity to discuss his theory in what I think is a very readable paper, and one worth the time.

He starts by saying that the relation between r, the rate of return to capital, and g, the rate of growth in the overall economy, are not predictive. They cannot be used to forecast the future, and are not even the most important factor in rising wealth inequality. The crucial factors are institutional changes and political shocks. Neither can the relation tell us anything about the decrease in the labor share of national income. He points to supply and demand for skills and education in this paper, as he does in his book, but this is a at best an incomplete explanation, owing more to the neoliberal view that the problems of workers are their fault than to a clear understanding of social processes in the US. A better explanation lies in tax law changes, changes in labor law and enforcement of labor law, rancid decisions from the Supreme Court, failure to update minimum wage and related laws, and government support for outsourcing and globalization.

What the theory does say is the subject of Part II.

I now clarify the role played by r > g in my analysis of the long-run level of wealth inequality. Specifically, a higher r − g gap will tend to greatly amplify the steady-state inequality of a wealth distribution that arises out of a given mixture of shocks (including labor income shocks).

In other words, as the raw number r – g increases, wealth inequality reaches a limit at a higher level, and income and wealth mobility become lower.

The important point is that in this class of models, relatively small changes in r − g can generate large changes in steady-state wealth inequality. For example, simple simulations of the model with binomial taste shocks show that going from r − g = 2% to r − g = 3% is sufficient to move the inverted Pareto coefficient from b = 2.28 to b = 3.25. Taken literally, this corresponds to a shift from an economy with moderate wealth inequality — say, with a top 1 percent wealth share around 20–30 percent, such as present-day Europe or the United States — to an economy with very high wealth inequality with a top 1 percent wealth share around 50–60 percent, such as pre-World War I Europe.

The inverted Pareto coefficient β is a measure of inequality used by Piketty and his colleagues. Here’s how he explains it in this paper:

That is, if β = 2, the average income of individuals with income above $100,000 is $200,000 and the average income of individuals with income above $1 million is $2 million. Intuitively, a higher β means a fatter upper tail of the distribution. From now on, we refer to β as the inverted Pareto coefficient.

The theoretical basis for this result can be found here, where Piketty and his colleague Gabriel Zucman provide a typical economists mathematical explanation. I’ve read some of this paper, but it is tough going.

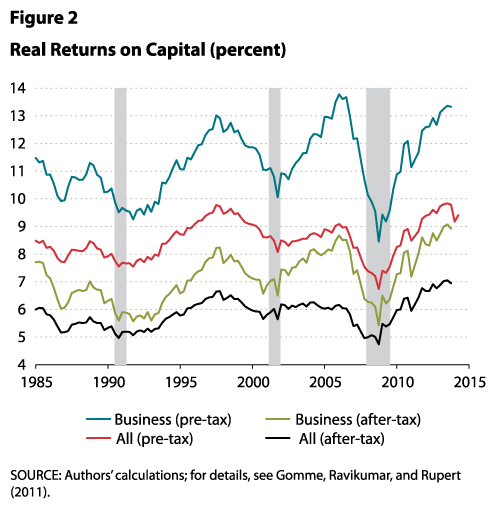

The returns to capital, especially business capital, are quite a lot higher than the levels given in Piketty’s example. Here’s the chart:

The returns to all capital after tax are about 7%. Paul Krugman put up a blog post saying that a realistic growth rate is about 2.2% at best for the next few years. This gives a difference r – g = 4.8%. Then using the equations on page 1356, we get an estimate that the inverted Pareto coefficient would be in the range of 11, which is a lot higher than the levels Piketty uses in the quoted material. By way of comparison, with that number, the average wealth of people with more than $10 million net worth would be $110 million. In the example Piketty gives for the top .1% with β =3.25, the figure would be $32.5 million.

Piketty notes that these coefficients are a rapidly rising function of r – g, which is apparently the case. In a recent paper, Emmanuel Saez and Gabriel Zucman estimate that the top .1% has a wealth share of 22% as of 2012, and there is every reason to think that has risen.

With Piketty’s general rule standing alone, there is no obvious limit to the level of wealth inequality, but in practice there are many practical reasons that it will level off. Some people will have more children, so the fortunes are divided into smaller shares. Some are lucky in investments and others aren’t. There are external shocks, wars and depressions. There are divorces, which split fortunes. Some people are able to earn high levels of labor income on top of capital income, increasing their wealth. Some die early, so their offspring are forced to spend more of their capital income to preserve their existing level of consumption. Others have expensive tastes and spend too much. These external forces eventually bring about a more or less static level of wealth inequality. Overall, this static level is higher when the fraction g/r is lower.

The time periods in the theoretical models used by Piketty and his colleagues are generational, they run 30 years. The big changes in wealth inequality began in the 70s, I’d guess, but became prominent enough that they were noticed in the late 80s and early 90s as the Reagan/Bush era tax cuts took hold, and regulatory structures were dismantled. By 2000, the final touches of formal deregulation were complete, and the Bush administration stopped enforcing most remaining laws leaving capital accumulation without restraint from legal pressure. It’s been about 15 years with little change, about half a cycle. The results follow the line Piketty and his colleagues predicted, and every year the new data supports their theories.

From this we can see that the coming empirical test is the maximum level of wealth inequality, or to put it another way, it’s a test of the downward pressures on the limits of wealth accumulation.

As a nation we have only taken the smallest possible steps to stem that tide, such as slow increases in the minimum wage, and tiny increases in taxes on the wealthiest to the extent they choose not to evade taxation in all sorts of allegedly legal ways. Neither of the presumptive candidates has any intention of making the kinds of changes necessary to change the outcome.

That brings us to the second empirical test: the level of wealth inequality that a civilized nation will accept before demanding change.

Or maybe the test is whether we are so cowed we won’t ever make any demands on our new lords and masters.

Update: for more on the uselessness of tweaks to the current system, see this interview by the excellent Lynn Parramore with Lance Taylor.

“Or maybe the test is whether we are so cowed we won’t ever make any demands on our new lords and masters.”

Cowed by what? The sheer weight of junk ideology? The virtual impossibility of organising workers into unions? The instant response-to challenges by the poor- of legislatures in the pockets of an aggressive and politically conscious ruling class? The constant surveillance of state organs at the bidding of the economic elites? The brutal policing of a wide variety of agencies-laughingly called law enforcement- charged with the task of keeping the 99% in their place?

Or all of the above dissolved into racism and served as Kool Aid?

The problem will not be solved by economics:

Howard Zinn

“Civil disobedience is not our problem. Our problem is civil obedience. Our problem is that people all over the world have obeyed the dictates of leaders…and millions have been killed because of this obedience…Our problem is that people are obedient allover the world in the face of poverty and starvation and stupidity, and war, and cruelty. Our problem is that people are obedient while the jails are full of petty thieves… (and) the grand thieves are running the country. That’s our problem.”

Consider the power of the 0.1% now, and keep in mind that only they have access to AI which is orders of magnitude beyond anything you’ll ever see on your smart phone.

quote”Our problem is civil obedience. Our problem is that people all over the world have obeyed the dictates of leaders…and millions have been killed because of this obedience…Our problem is that people are obedient allover the world in the face of poverty and starvation and stupidity, and war, and cruelty. Our problem is that people are obedient while the jails are full of petty thieves… (and) the grand thieves are running the country. That’s our problem.” unquote

Until the food chain is disrupted.

http://modernsurvivalblog.com/systemic-risk/the-majority-of-you-will-die-in-a-food-supply-collapse/

Cities only have a 3 day maximum supply at any given time. Should something happen… insurrection will make economics moot. Meanwhile..yeah..the Dumbest Country on the Planet remains obedient. We’ll see if they remain so if Trump becomes our Emperor.

The quote you site is Howard Zinn. It really doesn’t make much difference who is elected. The Imperial US has 3+ trillion dollars of war machinery deployed on the peripheries of China and Russia and essentially have hegemony over the rest.

In addition they have AI vastly more powerful than us hoi polloi, what chance do we have really – maybe a little if people act but they won’t so our children and grandchildren will be savage slaves if they live at all.

Howard Zinn was chillingly and clearly right.

Lots of questions, not enough answers. Here’s a piece reciting a progressive’s angst about taking Uber, for convenience, rather than a licensed/regulated taxicab. Forgetting all the arguments about whether Uber drivers are better off with or without us riders, it’s a nice exposition of a small slice of what people are up against when they try to address “inequality” on a daily basis.

.

http://www.theguardian.com/commentisfree/2016/may/22/uber-airbnb-convenience-liberals-pew-survey

Yes, intimidation has been part of American governance since Hamilton and Washington last visited the Forks of the Ohio. The neoliberal catechism that we are isolated seekers of pleasure and avoiders of pain is wrong; it is propaganda designed to achieve social submission. The catechism is ancient, as is the goal.

But Zinn was right not because he correctly described the problem. He was right because he saw that solutions to it were possible. We don’t need to wobble into obscurity. We do need to overcome the built-in propensity to follow the leader, regardless of what cliff s/he may invite us to topple over – for our security and benefit.

quote”We don’t need to wobble into obscurity. WE do need to overcome the built-in propensity to follow the leader, regardless of what cliff s/he may invite us to topple over – for our security and benefit.”unquote

Who is this ..WE.. you speak of? Can I depend on you to start this so called..”overcoming the built-in propensity to follow the leader”? Or should I just wait and see who has the fucking balls to start it..like the rest of the Dumbest Country on the fucking Planet.

Insert double rolling eyes smiley here.

Sounds like you’d much rather wait and see. Go for it.

(And when you quote, indicate that changes are your own; that’s the way WE do it.)

I would add that humans, like all living organisms, are distributed on a Gaussian scale: that is, most of us, if not a vast majority, share almost identical intellect at birth. So the entire notion, which isn’t just in America, that leaders are ‘special’, ‘smarter’, is simply, statistically and realistically speaking, untrue.

And this ‘propensity to follow the leader’ is not inherent. It is systemically introduced. I recall, in my early childhood, teachings about the early history of the US in which Presidents were akin to Gods, and that the Founders were an almost mythical group that wanted ‘freedom’ ‘prosperity’ (for all). All of these words, inspiring worship and awe from those with really no experience for comparison. Thank god my parents were avid scholars, and I took to reading outside the classroom. I remember having an epiphany in High School about how, really, all these notions of Great People, especially as they are taught in schools, are embellished to the point of legend. Actual biographies tell a completely different story, often rife with the obvious – that those born with not greater smarts, but in a higher class/caste/group tend to agglomerate to their kind and thus rarely fall to the state of commoners and have a wildly different reality than the rest.

As for Piketty’s general analysis, it seemed rather obvious and bland, not to mention narrow. In most of his economic theories, the concept of ‘other countries’, which I would term ‘another dimension’ for sake of mathematics, are always lacking. The main benefactors of ‘r’ are those in the higher echelons of society, yet today in the inter-connected global world, they are essentially above the laws and ties of any one nation because they do not really belong to any one nation. Their allegiance is to the power of wealth, no matter how or where it is derived, and no matter who is disadvantaged, as long as they are to gain.

I would like to see how these equations (maybe generalities is a better term) would hold if we added another dimension instead of focusing solely on a single entity/country. For example, how would adding China, with completely separate views, laws, etc. affect the overall conclusions drawn by Piketty? Is the current modern trends of America not closely tied to its largest bond holder and trading partner?

As a mathematician, I find these economic analysis to usually misrepresent factors because of the narrow lens through which they look – in this case, US over 200 years. Much of the wealth derived today is through trade, offshoring (which could be called ‘wage suppression’), and manipulation of markets. In the US, not only have we seen a wealth concentration in the upper class, but also a consolidation of so called mega-corporations, which dominate their respective industries. So not only do we have, at a high level view, less controllers with more control, but we also have less competition with more volume at stake – volume being the predictor of scale.

In my view, it is the consolidation of industry (due to multiple sources – lack of regulation, perversion of government and corporate interests/rise of lobbyism, etc) that ultimately lead to Piketty’s conclusion that as Beta increases, inequality essentially becomes more unequal. This makes sense at a logical standpoint, since as an industry has less competition, and as corporations get larger, their political weight grows and their competitions chances of competing diminish, essentially leading to a feedback loop where one company stands not just dominant, but monstrously dominant in both profits, but more importantly, in areas that the competition cannot reach such as taxes and regulatory bodies. In addition, as they grow their share of the market grows, and this market isn’t just domestic, but international. So what we have is not just wealth inequality among individuals, but a concentration in the markets which ultimately cause more harm as markets limit individual mobility far more than individual wealth (and the benefits gained from it).

Just my 2 cents.

1. We can think of your early training as part of the inculcation of what Foucault calls governmentality, the effort of society to pass along its values to the next generation, to prepare them for participation in society and especially in the production side of society, and to lay down the minimum standards for all to follow. Like any such orientation, it is aimed at what we think are our highest values, and are intended to serve as a mythological framework for our participation. For those not familiar with this idea, here’s a pretty good paper on the issue, especially the introductory section: http://www.thing.net/~rdom/ucsd/biopolitics/NeoliberalGovermentality.pdf This is largely the framework I am trying to teach myself for thinking about our situation, and in thinking about the ideas in the old books I read and write about.

.

2. Piketty’s ideas are bound to the economies he studies. You say they seem bland, but mainstream economists have totally ignored this field with minor exceptions. Krugman said that until Piketty came along and clarified the thinking on these models, mainstream economists couldn’t deal with inequality because they had no working models. I think the ideas are sketched out, and if you have the time, you might check out the paper at the first link. It contains a lot of the same material as Capital in the Twenty-First Century, but towards the end, he gives his model and a derivation. I think you will find your perceptions confirmed. The model is simple, and the explanations are very basic. Most important, like most economists he offers nothing on fraud and corruption, or on raw economic power in the model. That failure makes the models conservative, and given the level of growth they show, that’s scary.

.

That’s not to say he doesn’t deal with power, at least. As I read the book, power seemed to me to be very important, if not decisive, in understanding the causes of inequality.

.

In future posts, I will look at these issues in more depth.