Gary Shapley’s Notes Show That Gary Shapley Misrepresented David Weiss

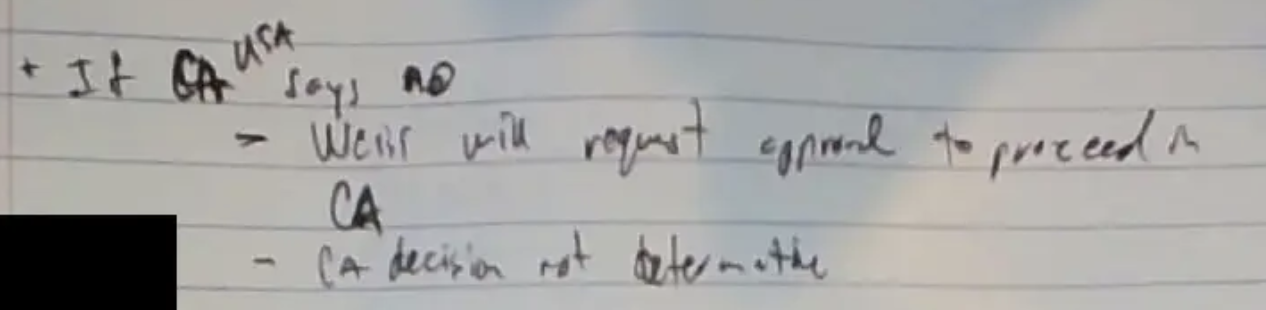

When Gary Shapley wrote down what was said about charging Hunter Biden with tax crimes in California at a contested meeting on October 7, 2022, he quoted Weiss as saying that if the US Attorney declined to prosecute, Weiss, “will request approval to proceed in CA” [my emphasis].

When Shapley relayed what happened in the meeting to his boss around six hours later, he described that Weiss “would have to request permission,” [my emphasis] even while admitting he was “unclear” on what Weiss said about where he’d get that permission.

Shapley’s lawyers shared these handwritten notes, over three months into his media tour with the right wing congressional set, because they think the fact that Shapley wrote down his understanding that Weiss said, “he is not the deciding person” [the latter part of which is redacted in the hand-written notes], that they disprove the testimony of others at the meeting.

The Special Agent in Charge, Thomas Sobocinski, said that both before and after the meeting, he understood Weiss to be the final decision-maker.

But this discrepancy later in his notes — Shapley’s replacement of “will” with “would have to,” his replacement of “approval” with “permission” — instead reveals that Shapley misunderstood what was said in the meeting, and then misrepresented what happened both that same day, with his supervisor, and ever since, with dumb right wingers in Congress.

To be sure, both versions are consistent with what David Weiss and Merrick Garland have been saying all along — including to Jim Jordan in June and to Lindsey Graham in July: that if Weiss decided to bring charges outside Delaware and the local US Attorneys didn’t want to partner on the case, he could ask for Special Attorney authority under 28 USC 515 and Garland would grant it. Both versions are consistent with the process Weiss has laid out. You ask the local US Attorney, and if they say no, you get Special Attorney authority.

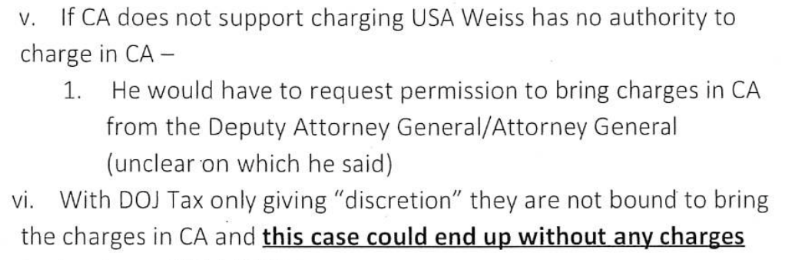

But in the notes Shapley took in the meeting, he recorded Weiss committing to taking the steps to charge the later tax years — the ones that had to be charged in Los Angeles, two of the three years that were part of the plea deal. In his email to his supervisor, Shapley transformed that into his panic that, “this case could end up without any charges,” [emphasis and panic Shapley’s], something that was sharply at odds with the commitment Shapley had recorded Weiss making in the meeting — will — to follow the process necessary to charge the case. Plus, Weiss’ description of seeking “approval” rather than “permission” substantially disproves Shapley’s claim that anything said at the meeting was “inconsistent with DOJ public position and Merrick Garland testimony.” Shapley had to reword what he originally recorded Weiss as saying to support that claim.

That he did so — that he rewrote his own notes to match his belief, and then shared the rewritten version rather than the original with Congress — damages his credibility rather than backing it.

To be sure, neither set of notes is reliable.

For example, there is at least one thing missing from Shapley’s hand-written notes that he records in the email to his boss: the substance of his objection to David Weiss’ decision not to charge the 2014 and 2015 tax years.

I stated for the record, that I did not concur with that decision and put on the record that IRS will have a lot of risk associated with this decision that there is still a large amount of unreported income in that year from Burisma that we have no mechanism to recover.

Shapley’s claim may not be (or may no longer be) true: at the plea hearing, AUSA Leo Wise stated that there was no restitution owed. But I have no doubt Shapley did make this objection. If he didn’t record making a statement he thought to be that important, then, what else did Shapley say that he didn’t write down?

More importantly, what did Shapley not say that he didn’t record?

There’s nothing unredacted in Shapley’s notes recording Sobocinski’s question — which Shapley included in his email to his boss — about whether there was any problem on the case with politicization.

FBI SAC asked the room if anyone thought the case had been politicized — we can discuss this [if] you prefer.

That’s important because, at least per Sobocinski’s interview with the Committee, no one raised concerns about politicization at the meeting. “I was asking in a room of leaders on this case to say, ‘Hey, we are working together. We’re moving this thing

forward. Do you think there’s any manipulation from the outside that’s stopping us from what we’re doing?'” Sobocinski told the House Judiciary Committee about the question. And, at least per Sobocinski’s representation, “nobody in that room raised their voice to say anything other.”

So unless the redacted lines at the end of Shapley’s notes record Shapley providing some kind of affirmative answer, then there’s no evidence he took the opportunity to express the wild claims of politicization he was making contemporaneously, but he also didn’t record himself passing up that opportunity. At least per Sobocinski’s memory, the SAC gave him an opportunity to air those concerns and he didn’t take it, an opportunity that might have elicited a very simple explanation about what Shapely was misunderstanding about how the Special Attorney process worked and might have saved us from all the theatricality that threatens all charges against Hunter Biden now.

Indeed, whether or not Shapley said anything in response to Sobocinski’s question, the most suspect part of his email to his boss was an offer to discuss politicization in person: “we can discuss this [if] you prefer.” Both these documents are designed to provide for accountability, but Shapley appears to have declined to write down anywhere what his claims about politicization were, which would have made him accountable to his claims just like he wants to hold Weiss accountable for what he understood him to say.

Shapley reorganized his notes between the hand-written ones and the email in a way that changes their meaning, too.

Per his contemporaneous notes, the first thing discussed after the discussion about the leak was Weiss’ rationale for not charging 2014 and 2015, the two more substantive years that would have to be charged in DC. Once you’ve explained that, then whether or not Weiss got Special Attorney status for DC is significantly moot (2016 was only ever treated as a misdemeanor).

In his email to his boss, though, Shapley moved that discussion to after his argument, covering the DC charges, the LA charges, and the involvement of DOJ Tax Attorney, that Weiss didn’t have authority to charge. If Weiss had already explained his prosecutorial decision about the most problematic Burisma years — something Shapley’s hand-written notes record him has having done — then none of the other complaints about these years (that Weiss or Lesley Wolf let the Statutes of Limitation expire, that Weiss didn’t get Special Attorney authority in DC) matter. Shapely reorders his notes to hide the fact that the DC decision didn’t matter.

The LA decision mattered — the one about which Shapley originally recorded Weiss saying he “will” pursue Special Attorney authority if need be. The DC decision did not.

Just as important a problem for Shapley’s credibility is that for more than three months, Shapley has been claiming the email was his best record of the meeting, without distinguishing what parts of the email were his editorial statements and what parts a record of the meeting. That parts of the email reflected him editorializing should have been clear to anyone smarter than Jim Jordan; Shapley’s use of “I believe” and “in my opinion” are a big tip-off.

But it’s clear that Republicans have nevertheless treated the email, and all its bullet points, as a record of the meeting. That’s most problematic with the way Shapley recorded his understanding that Weiss had asked for permission to file in DC, permission which hadn’t been granted.

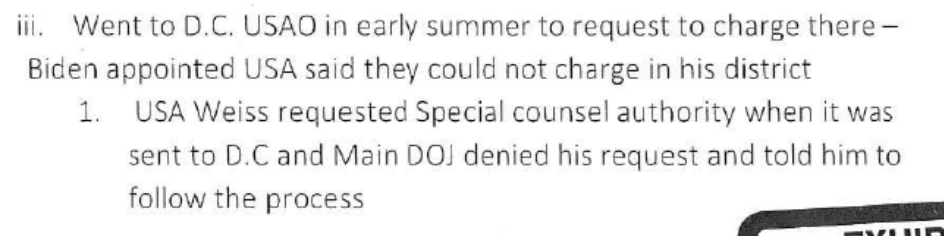

Staffers in Congress have been quizzing meeting attendees about things Shapley included in his email, without making clear they were background and not contemporaneous notes. One example that relates to the way Shapley packaged up his notes, at several points Steve Castor quizzed Sobocinski about whether he, “remember[ed] anything in that meeting about the fact that D.C. had declined to bring a case?” Sobocinski didn’t remember that — but likely for good reason. Shapley doesn’t record it as having happened, at all, in this meeting (and Sobocinski did not entirely back Shapley’s claim that that is what did happen). All Shapley recorded in his hand-written notes is that when Weiss asked for Special Attorney status (which Shapley lists as Special Counsel), DOJ — not Matthew Graves — told him to follow the process, which requires first asking if the US Attorney wants to partner on the case.

Even in these hand-written notes, this comment may have been editorializing; after all, Shapley records it after Weiss had already delivered his decision not to charge 2014 and 2015. But his hand-written notes definitely don’t reflect anyone saying that Graves had refused to partner on the case at the meeting.

In Sobocinski’s interview, he talked about how Shapley’s little media tour has created more challenges to actually charge this case, including threats against team members, particularly Lesley Wolf. There is nothing that Shapley has released publicly that helps the case and a great deal that will give Abbe Lowell more ammunition to demonstrate that the people pushing for tax charges against his client were going nuts because they weren’t allowed to violate rules on Sensitive Investigative Matters and because they didn’t understand bureaucratic process.

This is yet another example: Gary Shapley provided his editorialized version of a meeting that, he claims, was his red line to Congress and only months later did he share the underlying notes. Not only do the notes show he misrepresented what Weiss said about Los Angeles, but they raise yet more questions about Shapley’s equivocations about a leak that happened to coincide with a red line that isn’t entirely backed by his own notes. The motivated inconsistencies in the notes are the kind of thing defense attorneys use to discredit entire investigative teams, and Shapley has simply offered it up.

At this rate, Shapley’s media tour will be singularly responsible for making it impossible for Weiss to do the one thing Shapley claimed had to happen: charges against Hunter Biden.

Another very nice piece of exegesis.

[Welcome back to emptywheel. Please use the same username and email address each time you comment so that community members get to know you. I’ve edited your Name field this once to match your previous comments as I’m not certain you intended to use your RL name. Thanks. /~Rayne]

“Motivated inconsistencies” sums the whole mess up every elegantly.

I think the ability to charge Hunter Biden (and by extension Joe Biden) effectively is done. So instead, the RWNM and MAGA nuts in the House will try to scream this into reality like the swiftboaters did to John Kerry. The intersection of characters involved is substantial (no, I won’t enumerate) and the playbook well practiced. All it takes is a gullible media and compliant editors who lean conservative anyhow.

IF the courtier press actually pushes back, I’ll be surprised but it’s far more likely that the editors want a horse race and by golly they’ll create one if necessary.

So, the useful question here is how long can Weiss dangle a potential indictment sometime in the future knowing as he does that he’s got nothing that Abbe Lowell can’t ginzu into reasonable doubt if not blow up the ‘evidence’ entirely. Starr’s Whitewater snipe hunt sets the precedent, but I guess Weiss can go as long as the grand jury does. At what point does it end?

He can claim to be dangling 2018 and 2019 tax charges for another few years; SOL is 6 years.

But the gun charges will expire on October 12.

He CAN but will he?

Realistically can they bring a case with chain of custody issues; potential illegal searches; and misconduct (at best, at worst, criminal behavior) by investigators. Oh and BTW, HB’s previous attorney, will testify on his behalf about a signed agreement with Weiss.

And there they are, go to the post about it…

Question to Marcy re the first paragraph:

Weiss was at that point, and still is to my knowledge, the DE USA. Who is the USA Weiss was talking about there who might have declined to prosecute? Am I brain-farting another arm of the Hunter Biden investigation?

The prosecutors in the district the charges needed to be brought (they would be the prosecutors). Weiss was appointed 28 U.S. Code § 515 Special Attorney with 28 C.F.R. §§ 600.4 to 600.10 Special Counsel regs overlaid to get around the 600.3 non-government employee requirement, this allows him to work in other districts where he does not reside.

Thx. I was reading with blinkers on.

Oops, never mind. Just noted the “CA” in his handwritten notes. I glossed that, sorry.

CA has several districts, my guess it’s SDCA but whatever one handles LA.

CA has 4 federal judicial districts. LA is in the Central District.

Same district where Hunter resides, and is now suing Garrett (no relation to Joseph) Ziegler:

https://storage.courtlistener.com/recap/gov.uscourts.cacd.898532/gov.uscourts.cacd.898532.1.0.pdf

There is something I can’t seem to confirm from the various Shapley articles in the media. Did Graves and Estrada get to see the case that Weiss wanted them to partner on? All that gets reported is that they refused Weiss’ request to partner – leaving the presumption that the refusal was political in nature rather than based on the merits of the case they would be expected to help prosecute.

A timeline and explanation is in order. Something like: Weiss sent the case files to the DC and Central California districts on such and such date, along with his request to partner. The prosecutor for those districts declined Weiss’ request on such and such date. Maybe even some specifics included in their reply.

I’m not trying to be glib, but the reporting almost seems like Weiss said to them: “Hey, I want to charge the president’s son with several tax crimes. How about we partner up?”

Where is the missing stuff?

As noted, Sobocinski pointedly did not back Shapley’s claims on that front, but he wasn’t as close to it as Shapley.

There was a discovery review, which drew in Shapley’s emails, which he delayed for 8 months, which is why he decided he should become a whistleblower.

So Kevin McCarthy gave Jim Jordan and James Comer their frothy committees and let them stage their whistle-blower circuses for half a year, in the process actually undermining whatever shreds of “evidence” they might have mustered for their impeachment…of Hunter Biden.

This does not bode well for the success of the “inquiry” they have promised coming up.

Those two know how to produce bread and circuses for MAGA and get their faces on FAUX Nooze.

And…that’s about all.

No, it’s not quite all.

The RNC, NRCC, NRSC, various individual GOP candidates, and a non-trivial slice of the GOP superpac ecosystem have been raising money off of this quite nicely, thankewverymuch.

Yes, they want the cheers of the masses.

Yes, they want the eyeballs on conservative media outlets.

But mostly, they want the Benjamins so they can keep doing this ad infinitum.

Depressingly true, Peterr.

Shapley’s whistleblowing is bizarre because he was seeking a prospective conclusion of wrongdoing by his bosses. It is customary to write a memorandum that summarizes the meeting with all parties agreeing what was discussed. Hand written notes should be part of the memo.

I took tax accounting and worked in finance for years. I had my share of customers who had tax problems. From a tax accounting perspective, revenues and expenses are statutorily defined. Hunter Biden sends his return to the IRS and the IRS either accepts or audits it and reject it. The IRS can then determine if there was an honest misunderstanding or willful evasion. Biden then can dispute the IRS conclusions in tax court or make a settlement. The settlement normally ends the case. I re-read the IRS section 7201 regarding tax evasion and its handbook. An affirmative defense is “my bad, I didn’t understand what I did.” The IRS has to prove that the taxpayer had criminal intent.

What is ironic is that the Republicans are decrying the fortifying of the IRS’s auditing capacity while pursing a junkie for not paying his taxes through that same auditing capacity.

Not to mention their gleeful reaction to a gun charge they consider unconstitutional.