Hunter Biden Claims All Zhaos Look the Same to Joseph Ziegler

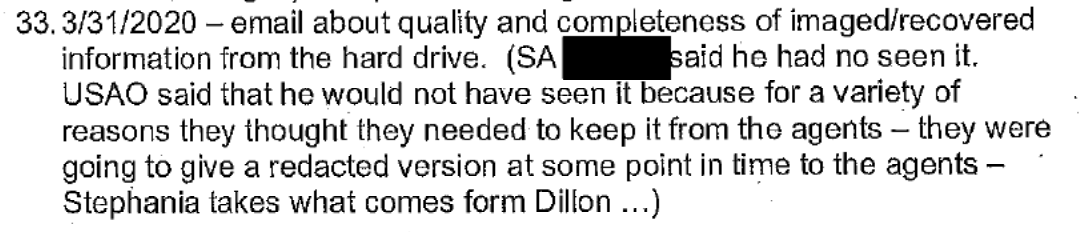

From the time Gary Shapley provided Congress obviously flawed summaries of WhatsApp texts, stripped of their identifiers, from an iCloud backup of Hunter Biden’s, I’ve argued their treatment reflects badly on the IRS agents involved.

When Abbe Lowell claimed, before Hunter was charged, that the IRS agents had gotten the identify of Hunter’s interlocutor wrong, I noted that the summaries, lacking identifiers, prevented what should be easy adjudication of this dispute.

The summary matters, a lot. That’s because Lowell claims that Shapley — or whoever did these summaries — misidentified the Hunter Biden interlocutor whose last name begins with Z.

In one excerpt that has now gotten a great deal of media attention, Mr. Biden is alleged to have been sitting next to his father on July 30, 2017, when he allegedly sent a WhatsApp message, urging the completion of some business transaction. See Shapley Tr. at 14. The inference is that the referenced message was being sent to an official of CEFC (China Energy) to forward a false narrative about the Bidens’ involvement in that company. The facts, which some media has now reported, are that President Biden and our client were not together that day, the company being referenced was not CEFC but Harvest Financial Group (with a person who also had the initial “Z”), and that no transaction actually occurred. More important, your own actions call into question the authenticity of that communication and your subsequent use of it. In short, the images you circulated online are complete fakes. Many media articles confirm that data purported to have come from Mr. Biden’s devices has been altered or manipulated. You, or someone else, did that again. All of the misstatements about this communication and your use of a false text are good examples of how providing one-sided, untested, and slanted information leads to improper conclusions. [my emphasis]

This is a remarkable claim, because — if true — it suggests the IRS was investigating Hunter Biden based on wildly incorrect assumptions about the identity of his interlocutors.

Abbe Lowell claims that the IRS agents who investigated his client for five years — the son of the President!!! — didn’t know to whom he was talking! I’ve heard a lot of outlandish claims from defense attorneys (though Lowell is far more credible than the grifters who defend a lot of January 6 defendants), But this is an utterly inflammatory claim.

Had Shapley used responsible summaries, rather than the unprofessional script he did use, it might be possible to figure out who is right, here, because then we could compare the actual number or email account used.

When Luke Broadwater tried to manufacture a partisan both-sides dispute out of this discrepancy, I noted the real conflict came between Republicans, some of whom said the Zhao in question was Henry, others who said it was Raymond.

The summary and the fabrications of the text and Smith’s use of the initials “HZ” matter because there’s a dispute between Republicans and their IRS source about the identity of the person involved.

Shapley said the texts involved Henry Zhao, consistent with Smith’s fabrication.

But in a later release, James Comer described the interlocutor as Raymond Zhao — which is consistent with the interjection in the summary (and other communications regarding this business deal).

On July 30, 2017, Hunter Biden sent a WhatsApp message to Raymond Zhao—a CEFC associate—regarding the $10 million capital payment:

As we’ll see, Broadwater predictably “fact checks” this as a dispute between Democrats and Republicans. It’s not. Before you get there, you first have to adjudicate a conflict between the guy who led the IRS investigation for more than two years, Gary Shapley, and James Comer. It’s a conflict sustained by the shoddiness of the underlying IRS work.

This is a story showing not only that James Comer and Jason Smith don’t know what they’re talking about, but are willing to lie and fabricate nevertheless, but even the IRS agents may not know what they’re talking about, and if they don’t, it’s because the standard of diligence on the investigation of Joe Biden’s son was such that they didn’t even include the identifier of the person to whom Hunter was talking, which would make it easy or at least possible to adjudicate this dispute.

In Wednesday’s hearing, after such time as they had received discovery on this material, Hunter Biden and Abbe Lowell provided a new explanation for the discrepancy: That the first text (but only the first text) was accidentally sent to Henry Zhao, and the follow-up texts — which were therefore necessarily unrelated — came from Raymond Zhao.

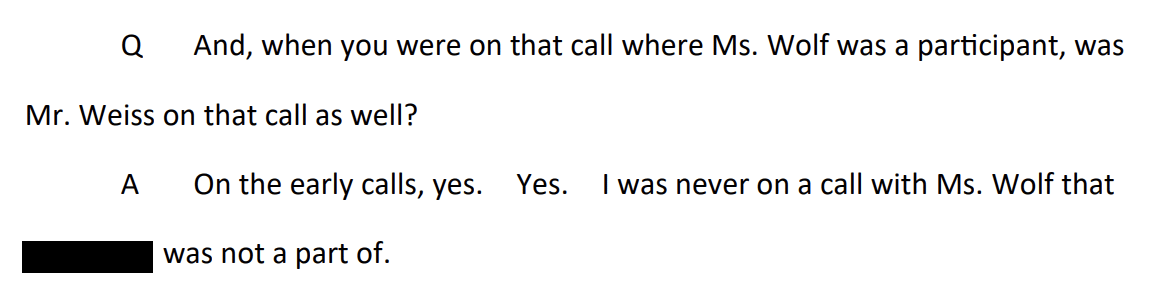

Q This is a giant text pack prepared by the IRS investigators, summarizing, and in many cases, quoting WhatsApp message.

Mr. Lowell. Do you have the underlying message?

[Redacted] We have this document. This is what we have.

Mr. Lowell. I want to point out on the record that is all known to you that we have great reservations about the accuracy and completeness of what two IRS agents who have decided to go on television and try to promote what they believe should happen to Mr. Biden as having made a complete record.

And when there have been records, they have not been complete?

And when they make summaries, they are often quoting from texts or communications, which appear to have been altered by those other than themselves.

So with all that, you can certainly ask your questions. But I do not accept the premise that what you’re about to ask him is either an authentic or authenticated or a complete document.

[Redacted]: Okay.

Mr. Lowell. With that in mind, let’s go.

[Redacted] Okay.

BY [Redacted]:

Q Just to set expectations here, I’m going to refer to three. Okay? Then we’ll be done with this document for now.

A Page 3?

Q I’m going to refer to three sort of topics —

A Okay.

Q — within this giant document, not 148. We’re not going to go through every page. I’m sort of managing your expectations here.

A Thank you.

Q I’d like you to turn to page 4, and it’s a message dated July 30th, 2017. It’s about halfway down the page and it begins, “WA message with SM.” And that’s the — that stands for Sportsman, and that’s what they called you, and Zhao. Have you identified the one that I’m referring to?

Mr. Lowell. It’s down the page. It’s the only one for the 30th?

[Redacted]. Correct.

Mr. Lowell. Okay. Yes.

BY [Redacted]:

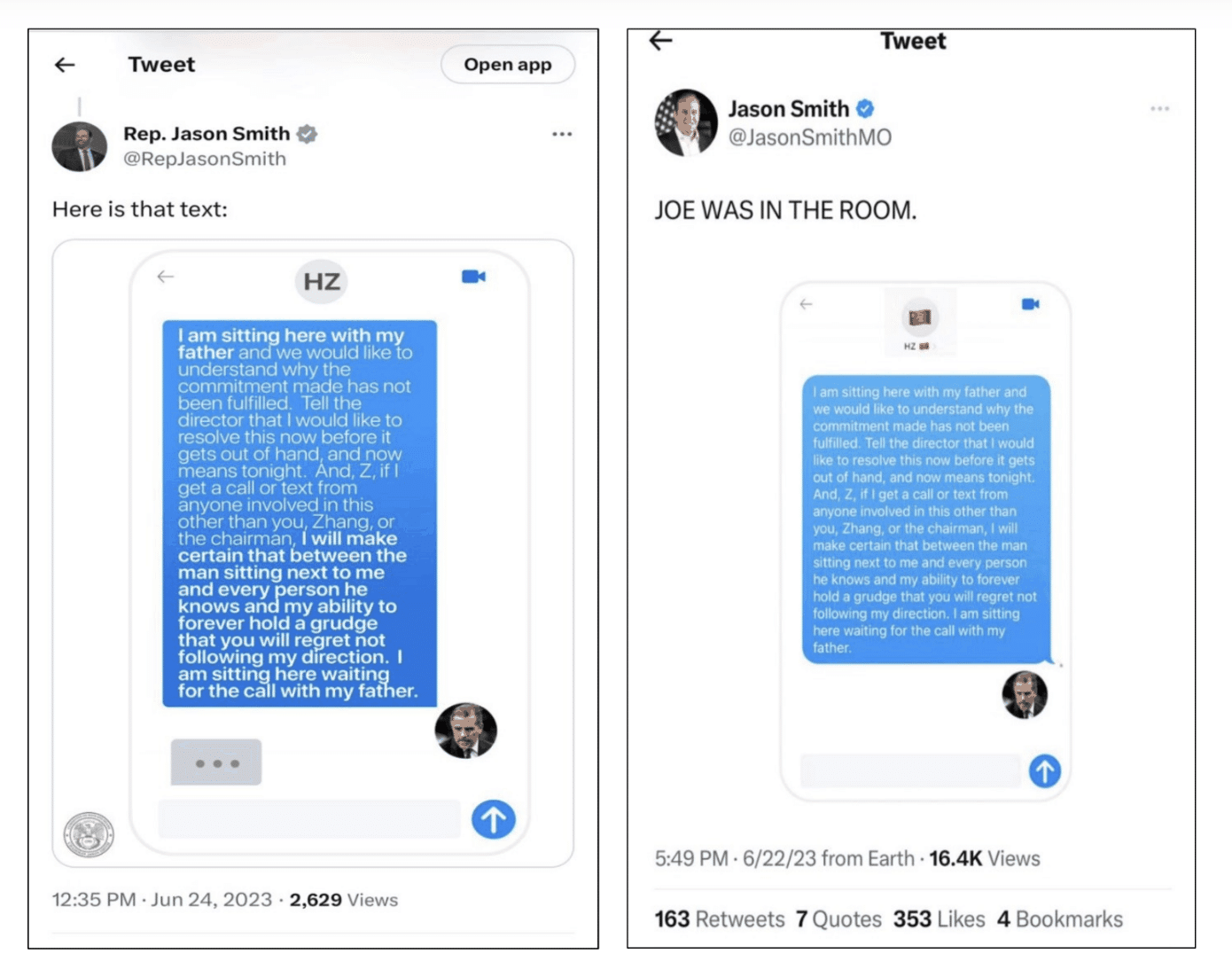

Q And so the text, according to the IRS, the Federal investigators, say, “Z, please have the director call me, moment James or Tony or Jim. Have him call me tonight. I’m sitting here with my father, and we would like to understand why the commitment made has not been fulfilled.

“I’m very concerned that the chairman has either changed his mind or broken our deal without telling me or that he’s unaware of the promises and assurances that have been made have not been kept.

“Tell the director I would like to resolve this now before it gets out of hand, and now means tonight. And, Z, if I get a call or text from anyone involved in this other than you, Zhang or the chairman, I will make certain that between the man sitting next to me and every person he knows and my ability to forever hold a grudge that you will regret not following my direction.

All too often people make mistakes — sorry.

“All too often people mistake kindness for weakness, and all too often I’m standing over the top of them, saying, I warned you.

“From this moment until whenever he reaches me. It’s 9:45 a.m. here and I assume 9:45 p.m. there. So his night is running out.”

Zhao responds, “Copy. I will call you on WhatsApp.”

You respond, “Okay, my friend. I’m sitting here, waiting for the call, with my father. I sure hope whatever it is are you doing is very, very, very important.”

Then Zhao says, “Hi, Hunter. Is it a good time to call now? Hi, Hunter, Director did not answer my call, but he got the message you just mentioned.”

A Yeah.

Q Do you have any recollection of sending these?

A No, but I’ve seen this and —

Mr. Lowell. Is there a question?

[Redacted]. Yes. Does he have a recollection of sending the message?

The Witness. And I do not, but I do know this. I have now seen it, which it’s been presented. I would say two things about this message.

Mr. Nadler. Can you speak up?

The Witness. I would say two things about this message. The first thing is this.

Is that the Zhao that this is sent to is not the Zhao that was connected to CEFC.

BY [Redacted]:

Q Okay.

A Which I think is the best indication of how out of my mind I was at this moment in time.

Again, I don’t — my addiction is not an excuse, but I can tell you this: I am more embarrassed of this text message, if it actually did come from me, than any text message I’ve ever sent.

The fact of the matter is, is that there’s no other text message that you have in which I say anything remotely to this. And I was out of my mind. I can also tell you this: My father was not sitting next to me. My father had no awareness. My father had no awareness of the business that I was doing. My father never benefited from any of the business that I was doing.

And so, I take full responsibility for being an absolute ass and idiot when I sent this message, if I did send this message.

Q Okay.

[Redacted]. When you say it wasn’t Zhao from CEFC, who —

Mr. Nadler. Would you speak up, please?

[Redacted]. Which Zhao are you referring to if it wasn’t from CEFC?

The Witness. The number that I believe it went to was to Henry Zhao. Zhao is a very common — it’s not a surname — surname in China. I mean, obviously, very common surname. And I, like an idiot, directed it towards Henry Zhao who had no involvement, who had no understanding or even remotely knew what the hell I was even Goddamn talking about. Excuse my language

BY [Redacted]:

Q And he seems to —

A No, no, no, no, no, the Zhao — it’s a different — you’re conflating now.

Q Okay.

A And this why this report from the IRS is absolutely wrong. They’re two different messages.

The Zhao that calls me is not related to the message that was sent. I speak to him the next day. They’re two completely different sets of messages. One goes a number because, I made the Goddamn — excuse my language again — because I made like an idiot, and I was drunk and probably high, sent a — this ridiculous message to a Zhao, to a Henry Zhao.

But then the next day, I speak to a Raymond Zhao, who has never received the message that Henry Zhao got. And so that’s why this report is very misleading in many ways.

Mr. Lowell. That’s exactly why I raised the point before you decided to ask questions. The IRS agents —

The Witness. I gave —

Mr. Lowell. — took two different times and two different messages and conflated them. That’s what he’s explaining.

The Witness. And I can — and we can show you that.

And I also could show you that on that message, there was never a Chinese flag and a picture of it, as I think was shown in the Oversight Committee before. [my emphasis]

If I understand it correct, Henry Zhao was involved in an earlier business deal, Raymond Zhao is the one with ties to CEFC.

Here’s how Shapley presented the text in his first deposition.

And here’s the exhibit on which House Republicans are likely relying.

There are still a number of inconsistencies with this story, but it really doesn’t make sense to address them without full context (which Hunter presumably has).

In any case, the text string is still somewhat damning to Hunter; his conversations with CEFC continued the same thread, cutting Tony Bobulinski and the others out of the deal.

But I will say this: I already have questions about where WhatsApp texts got saved, not least because at the time, having access to one WhatsApp instance would give you access to the rest of it.

All the more so given that, if we can trust the warrant and Joseph Ziegler’s description of the source of these texts (Apple Backup 3, which the warrant describes as an Apple 6S backup), the timing is curious. Hunter used an iPhone 6S much earlier than 2017, and he initiated a new one on February 9, 2019, just as his devices were packed up for delivery to John Paul Mac Isaac.

Whatever the explanation, it seems that rather than work through a discrepancy, or just leaving out texts that couldn’t be explained, the IRS just blew through inconsistencies.