The Origins of Totalitarianism: Interlude on The Commons

Previous posts in this series:

The Origins of Totalitarianism Part 1: Introduction.

The Origins of Totalitarianism Part 2: Antisemitism

The Origins of Totalitarianism: Interlude on the Tea Party

The Origins of Totalitarianism Part 3: Superfluous Capital and Superfluous People

In Part 3, I discussed two problems created by unrestrained capitalism, superfluous wealth and superfluous people. These twin problems are evidence of the damage done to people and societies by capitalism: the creation of large numbers of citizens with no role in the productive system of a nation-state, and the enormous wealth and power of the rich capitalists and the aristocracy. Arendt offers an explanation.

The decisive point about the depressions of [the 1860s and 70s], which initiated the era of imperialism, was that they forced the bourgeoisie to realize for the first time that the original sin of simple robbery, which centuries ago had made possible the “original accumulation of capital” (Marx) and had started all further accumulation, had eventually to be repeated lest the motor of accumulation suddenly die down. In the face of this danger, which threatened not only the bourgeoisie but the whole nation with a catastrophic breakdown in production, capitalist producers understood that the forms and laws of their production system “from the beginning had been calculated for the whole earth.” P. 148 fn omitted.

The motor of accumulation is a nice image for the idea that capital must move, must be constantly active, or it becomes useless and dangerous. The idea of the constant motion of money is similar to an idea we encounter later in the book, along with the idea of superfluity. The word “bourgeoisie” is slippery as commenter Bevin noted in response to Part 3, and can easily lead to confusion. For the purposes of the above quote, I think Arendt means the richest capitalists and aristocrats, and perhaps their financiers.

This is one of the footnotes I omitted:

According to Rosa Luxemburg’s brilliant insight into the political structure of imperialism {op. cit., pp. 273 ff., pp. 361 ff.), the “historical process of the accumulation of capital depends in all its aspects upon the existence of non-capitalist social strata.” so that “imperialism is the political expression of the accumulation of capital in its competition for the possession of the remainders of the non-capitalistic world.” This essential dependence of capitalism upon a non-capitalistic world lies at the basis of all other aspects of imperialism, which then may be explained as the results of oversaving and maldistribution (Hobson, op. cit.), as the result of overproduction and the consequent need for new markets (Lenin, Imperialism, the Last Stage of Capitalism, 1917), as the result of an undersupply of raw material (Hayes, op. cit.), or as capital export in order to equalize the national profit rate (Hilferding, op. cit.).

Here is the Wikipedia entry on Luxemburg. She was a revolutionary communist and a Marxist intellectual. Arendt refers to her book, The Accumulation of Capital, dated 1923, several years after Luxemburg was executed by the German Freikorps. I think Arendt might be referring to this book, and here’s a quote matching her description of Luxemburg’s thought.

Accumulation is impossible in an exclusively capitalist environment. Therefore, we find that capital has been driven since its very inception to expand into non-capitalist strata and nations, ruin artisans and peasantry, proletarianize the intermediate strata, the politics of colonialism, the politics of ‘opening-up’ and the export of capital. The development of capitalism has been possible only through constant expansion into new domains of production and new countries. But the global drive to expand leads to a collision between capital and pre-capitalist forms of society, resulting in violence, war, revolution: in brief, catastrophes from start to finish, the vital element of capitalism.

This analysis springs from Luxemburg’s reading of Marx, who, she says, was unable to show how accumulation of capital could occur in a purely capitalist system. Luxemburg says that accumulation of capital is only possible when the capitalist can find some new area to exploit. Arendt agrees.

I did not see any discussion of this issue in Jevons or in the bits and pieces of other 19th and early 20th century economists I have read, and I certainly can’t find it in the textbooks of Mankiw or Samuelson. Apparently this is not an issue of interest to economists. But the question does not disappear just because the self-described experts don’t want to talk about it. In The Great Transformation Polanyi describes the enclosure of the commons in England as a precursor to the Industrial Revolution. The enclosures were an example of the exploitation of a pre-capitalist strata made up of peasants and smallholders, to accumulate capital in the hands of the rich and vicious. One of the demands of the armed thugs in Oregon is that federal land, our joint land, be given to them for their personal exploitation and profit. They’re just more blatant than the Koch Brothers and Exxon.

One of the primary goals of neoliberals is to take over the commons. The medical system and wide swaths of the prison system have been turned over to the profiteers already. They play a huge role in the military state and the national security state. With the help of the rich and powerful, they are working to take over the education system with their charter schools and their for-profit colleges. They are all over the place, always scraping away at things we can do for ourselves cheaply and well through government, and routing taxes (which they don’t pay) and profits to themselves at the expense of the people who actually do the work.

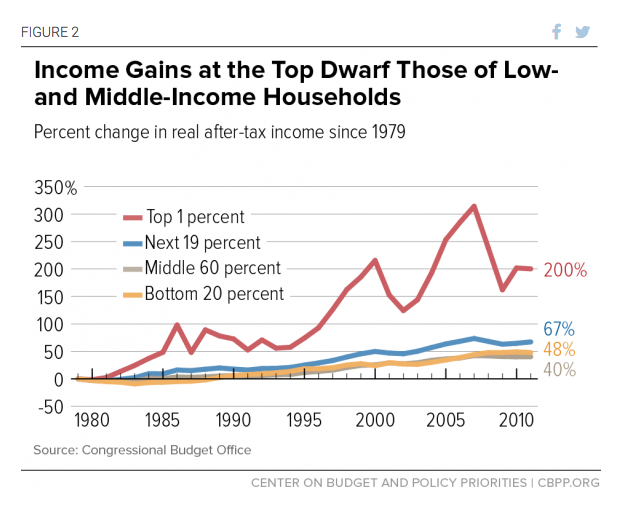

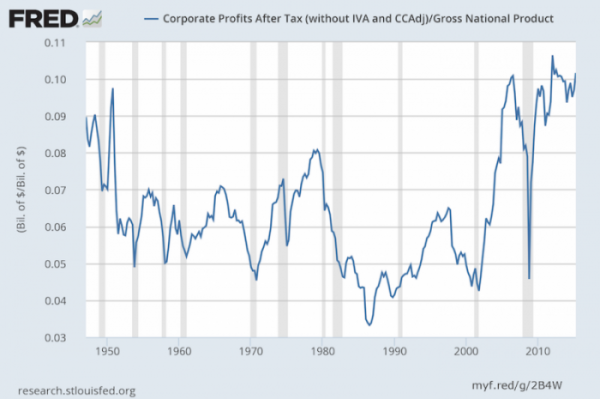

The facts today support the views of Arendt and Luxemburg. This is no surprise. The conditions today are similar to the unrestrained capitalism of the late 1800s through the 1920s, with monopolies, oligopolies, vast disparities of income and wealth, and a government responsive only to the demands of the rich.