There has been a lot of performed ignorance about the origin of the investigation that led to the felony conviction of Donald Trump.

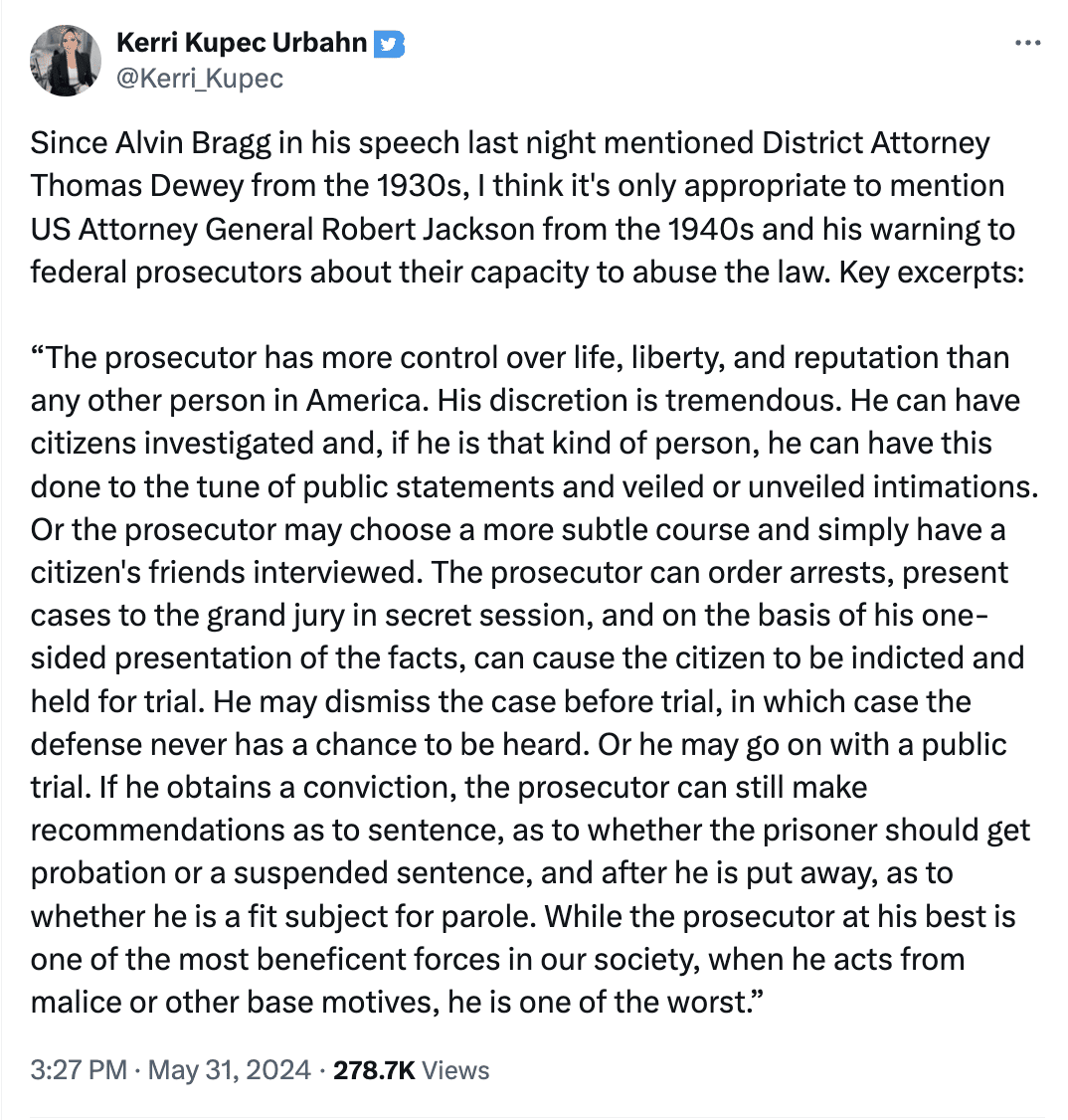

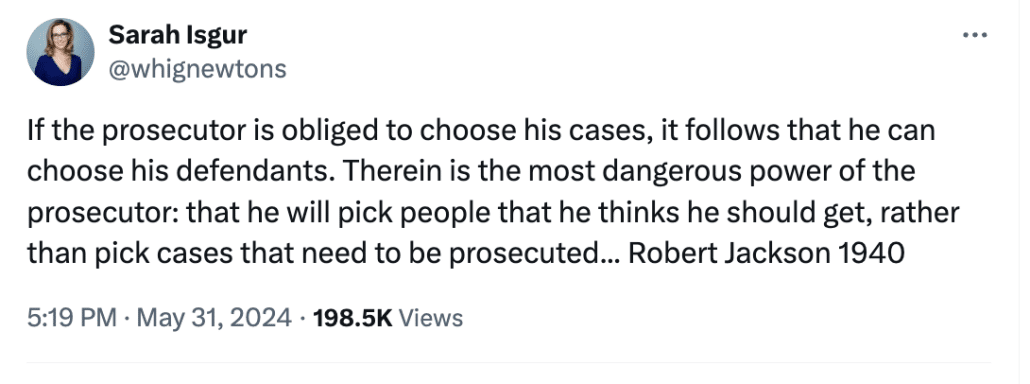

Former Attorney General Jeff Sessions’ spox, Sarah Isgur, quoted Robert Jackson about prosecutors choosing defendants.

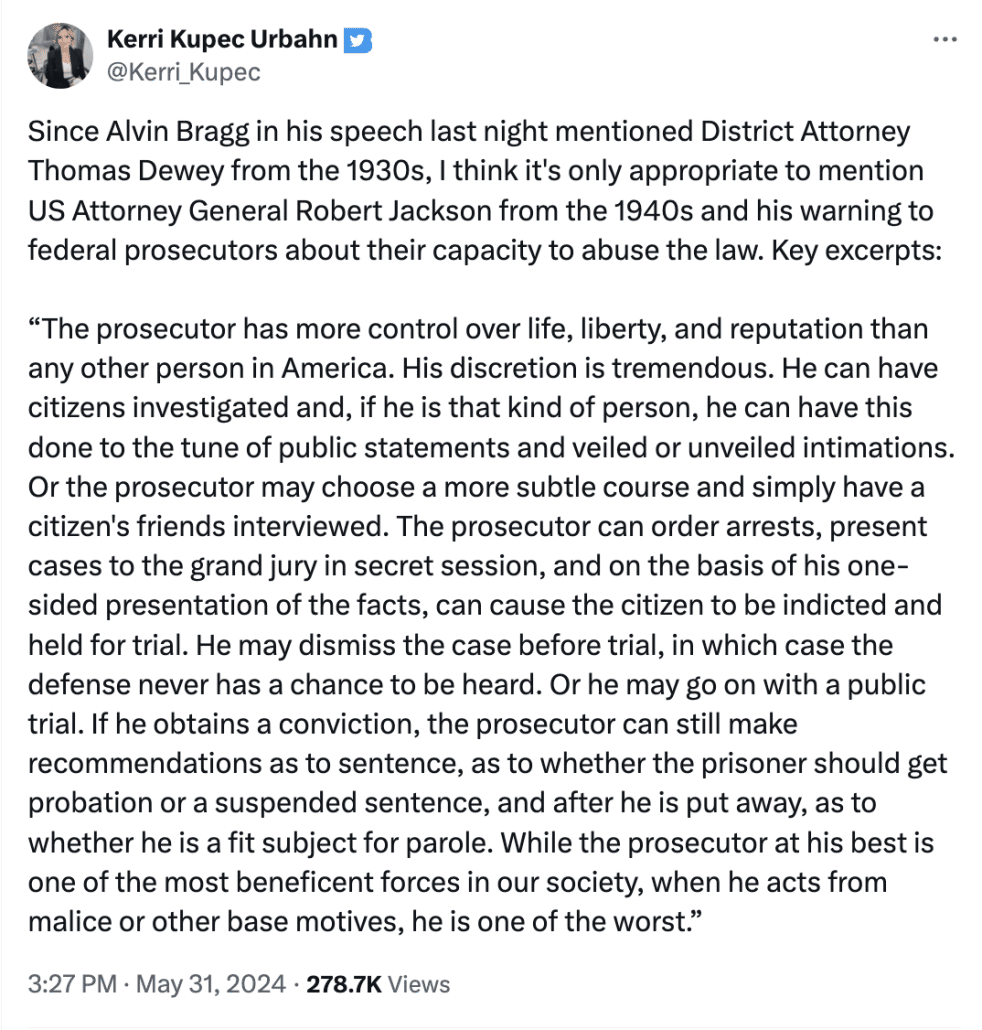

Kerri Kupec, the DOJ spox who helped Bill Barr spin key aspects of his unprecedented corruption at DOJ, likewise quoted Jackson.

Both mouthpieces for Trump’s DOJ insinuated that Alvin Bragg invented this case out of thin air, rather than pursuing the fraud revealed by an investigation that developed — and was substantially interfered with by Barr — while they were at DOJ.

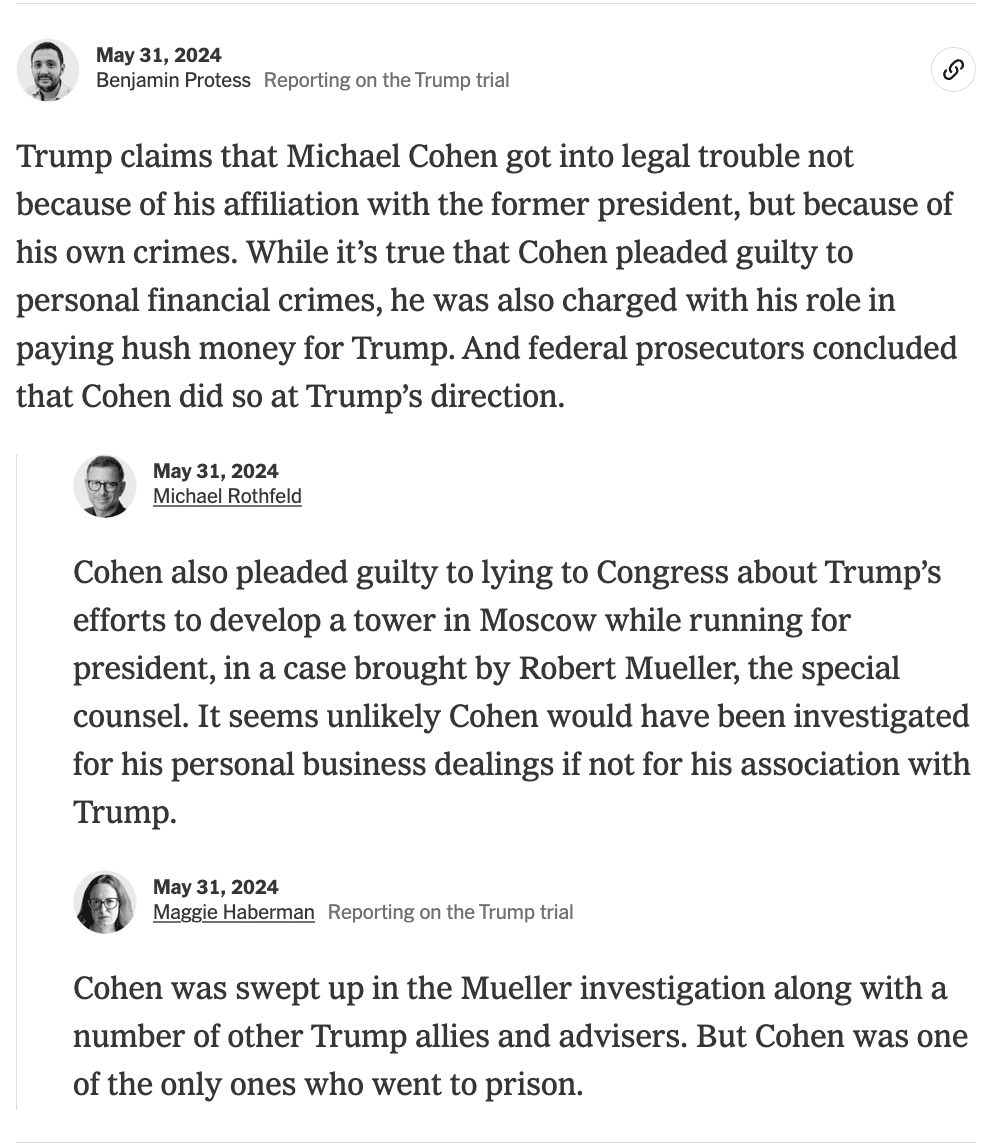

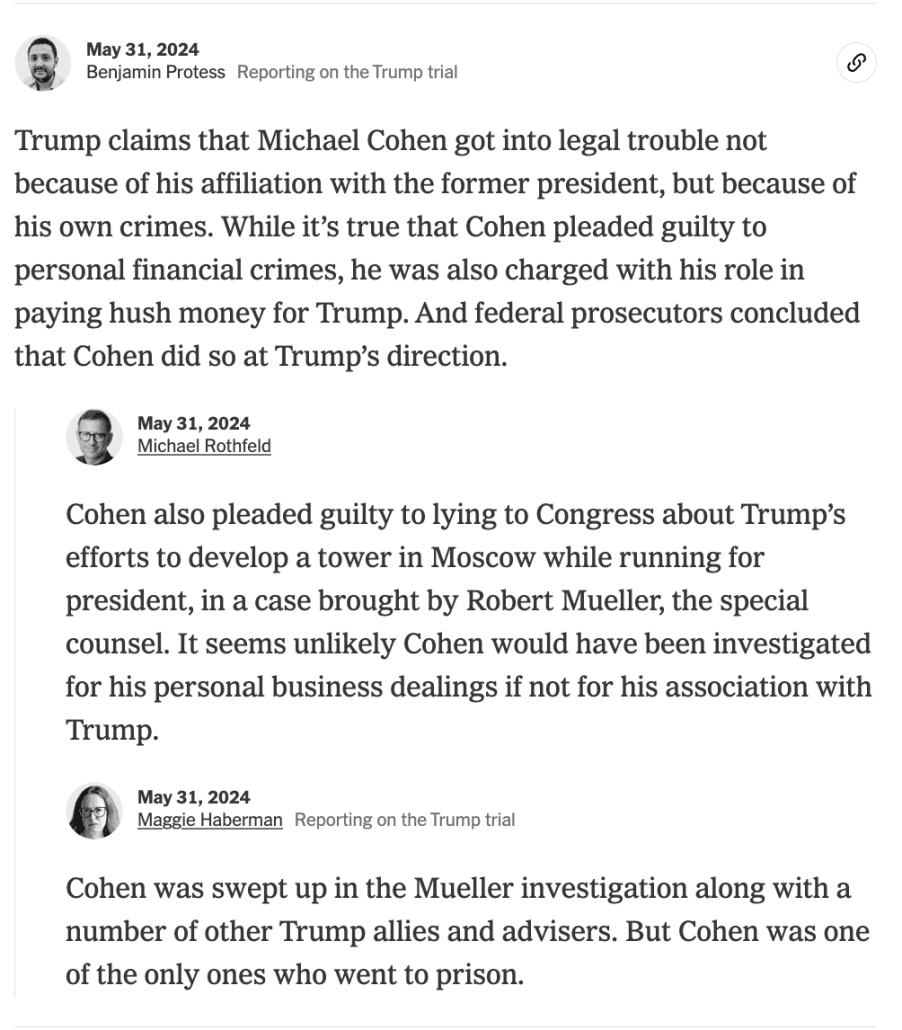

Then, three of the NYT reporters who commented on Trump’s wild screed the other day mused about whence this investigation might have come from, with Maggie describing those whose own actions made them targets of the Mueller investigation in the passive voice, “swept up,” as she is wont to do (to say nothing about her refusal to discuss the way Trump’s pardons silenced key witnesses against him).

We know whence the investigation into Cohen, and therefore the investigation into Trump, came from, thanks in part to a media coalition including NYT, because the coalition liberated the warrants used to investigate Cohen.

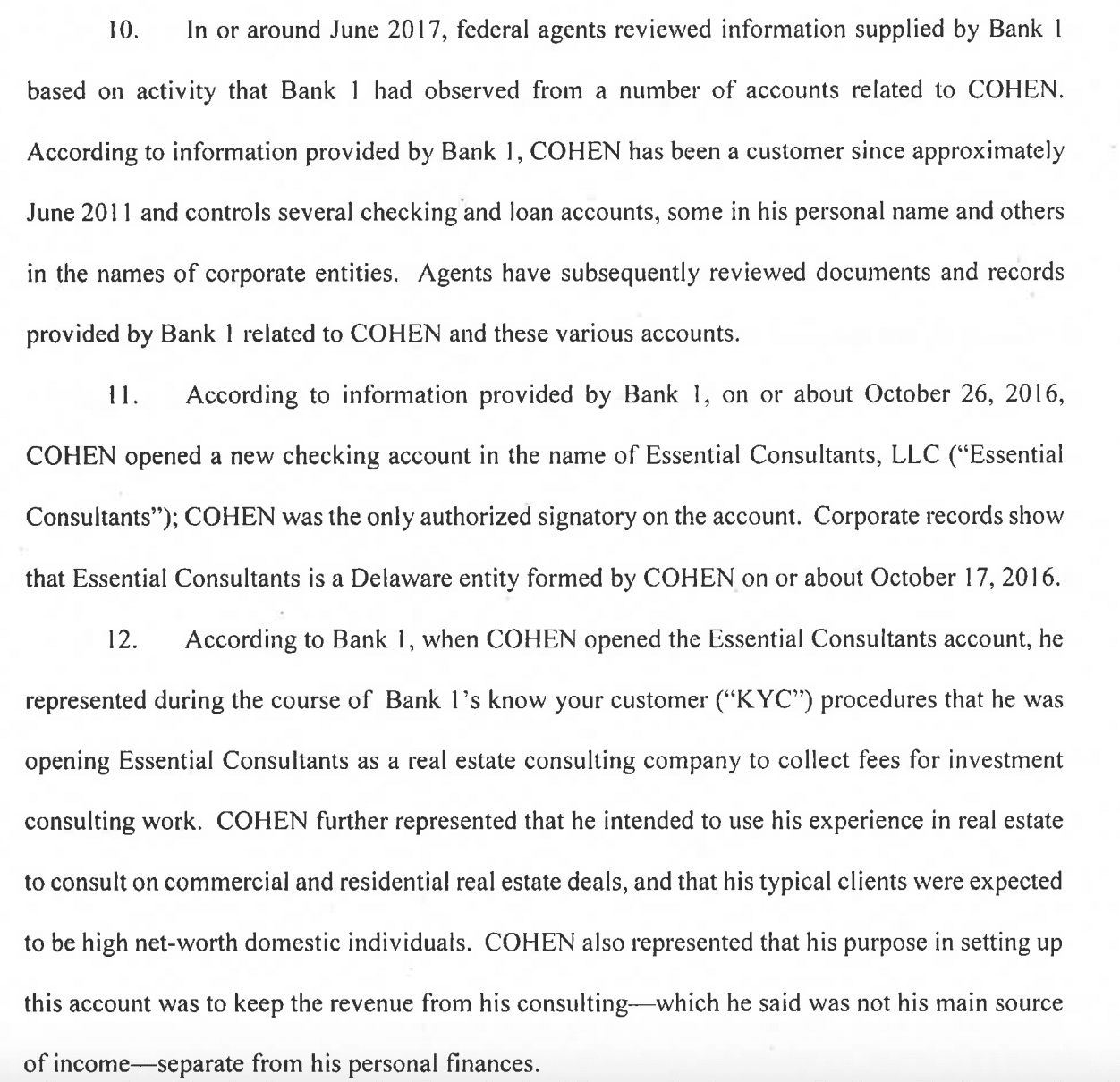

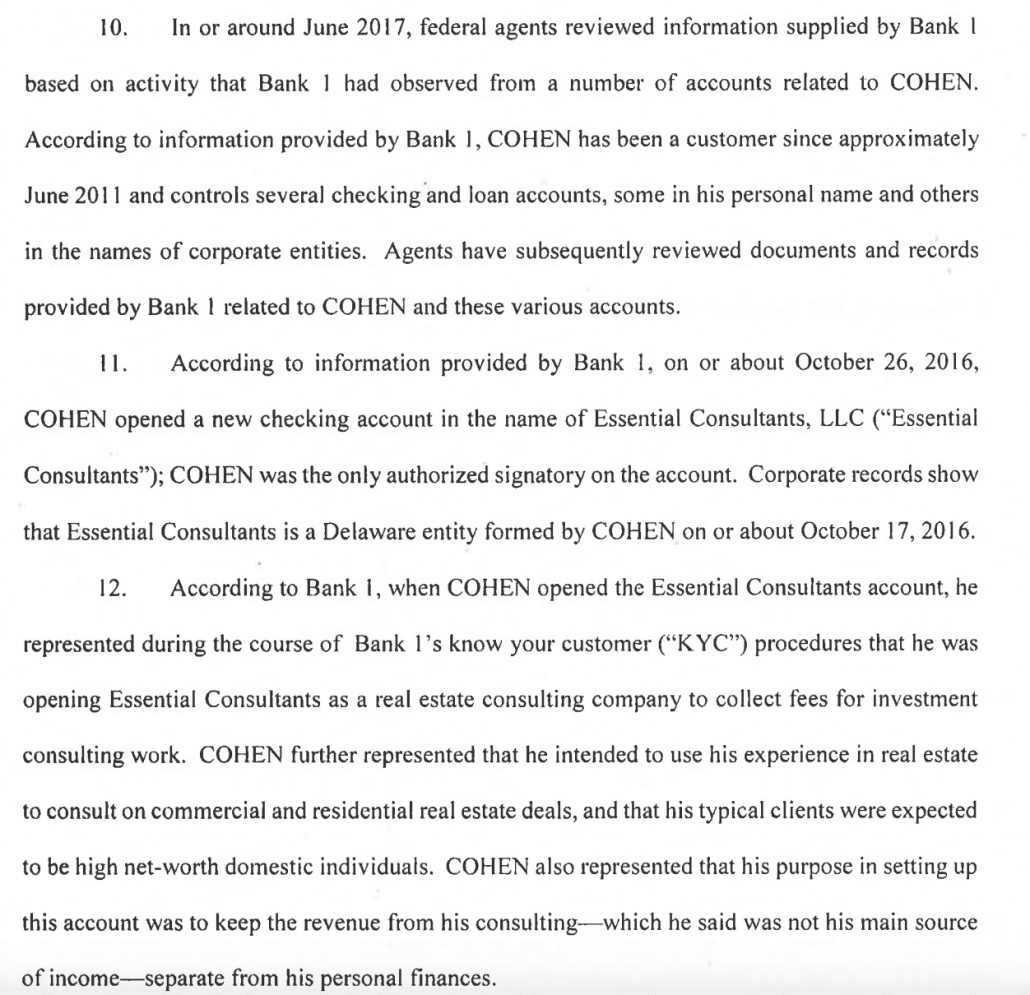

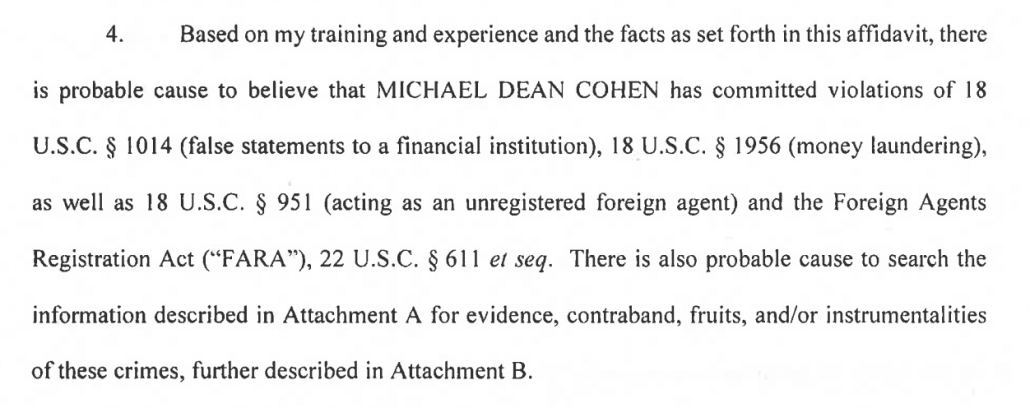

As the first warrant targeting Michael Cohen, dated July 18, 2017, lays out, the investigation started from information “supplied by” — almost certainly in the form of Suspicious Activity Reports — a bank known to be First Republic Bank.

This Know Your Customer filing was submitted as an exhibit at the Trump trial.

The entity will be set up to receive consulting fees in the form of wires and ACH — all under 10K 1-2 a month, the wires and fees will be income from consulting work from personal clients, all domestic. He will then internally transfer the funds to his personal account at First Republic. He is setting this account to keep the income from his consulting work separate.

Even the original Stormy Daniels payment violated the representations Cohen made in that KYC statement (as likely explained in still-redacted passages in the warrant affidavit).

As Gary Farro, a witness who had worked at First Republic explained at trial, Cohen denied that the account (and an earlier one, Resolution Consultants, the plan for which he abandoned) had anything to do with political fundraising.

Q Looking now at the question in — labeled number 12. What does that say?

A “Is the entity associated with political 21 fundraising/political action committee PAC.”

Q And what answer is checked?

A “No.”

Q And do you know why the form includes a question about political fundraising?

A Because it would be something the bank would want to know.

Q And if somebody checked “yes,” is that something that would require additional review by the bank?

A Yes, it would.

[snip]

Q And looking at the questions towards the top third of 3 the page.

In the form does it say — does this have the same question that we saw in the Resolution Consultants form?

It says: “Is the entity associated with political fundraising or political action committee.”

A Yes. This is just the digital form of what was provided earlier, which would be the hard copy.

Q What’s the answer to the political fundraising question 11 on the form?

A Is “No.”

Q Now, turning to the business narrative portion in the middle of the page.

What business narrative is provided for Essential Consultants LLC?

A It’s Michael Cohen is opening Essential Consultants LLC as a real estate consulting company to collect fees for investment consulting work he does for real estate deals.

Within days after he set up the account on October 13, 2016, his October 27 transfer to Keith Davidson violated Cohen’s claims to be engaging in real estate deals. As Farro explained, had Cohen indicated the transfer had a political purpose, it would have invited more scrutiny from the bank — and possibly a delay in the payment.

Q Did any of the wire transfer paperwork indicate that money was being transferred on behalf of a political candidate?

A No.

Q Would the bank’s process for approving the wire transfer be different if Mr. Cohen had indicated that the money was being transferred on behalf of a political candidate?

A We would have additional due diligence.

Q Would that have delayed the transaction?

A It certainly could.

Had it ended with just that hush payment, had the hush payment remained secret, Cohen might have gotten away with it.

But it didn’t.

As that first warrant goes on to explain, after Cohen quit Trump Organization and announced he was serving as Trump’s personal lawyer, he used the same account to accept payment from a bunch of foreign companies, some of them controlled by foreign governments. That led the bank to provide more information — again, almost certainly in the form of SARs — to the Feds.

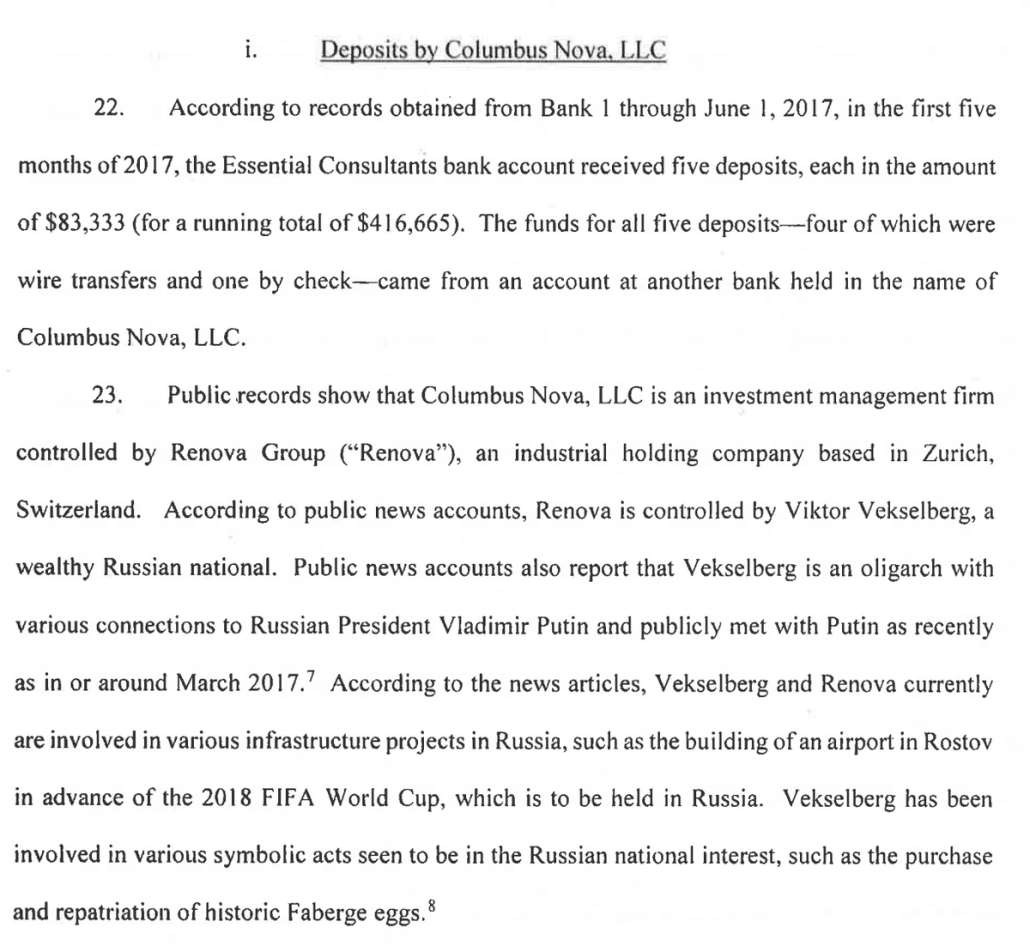

The most alarming of those payments involved $416,665 in payments over five months from Columbus Nova, which is ultimately controlled by Viktor Vekselberg.

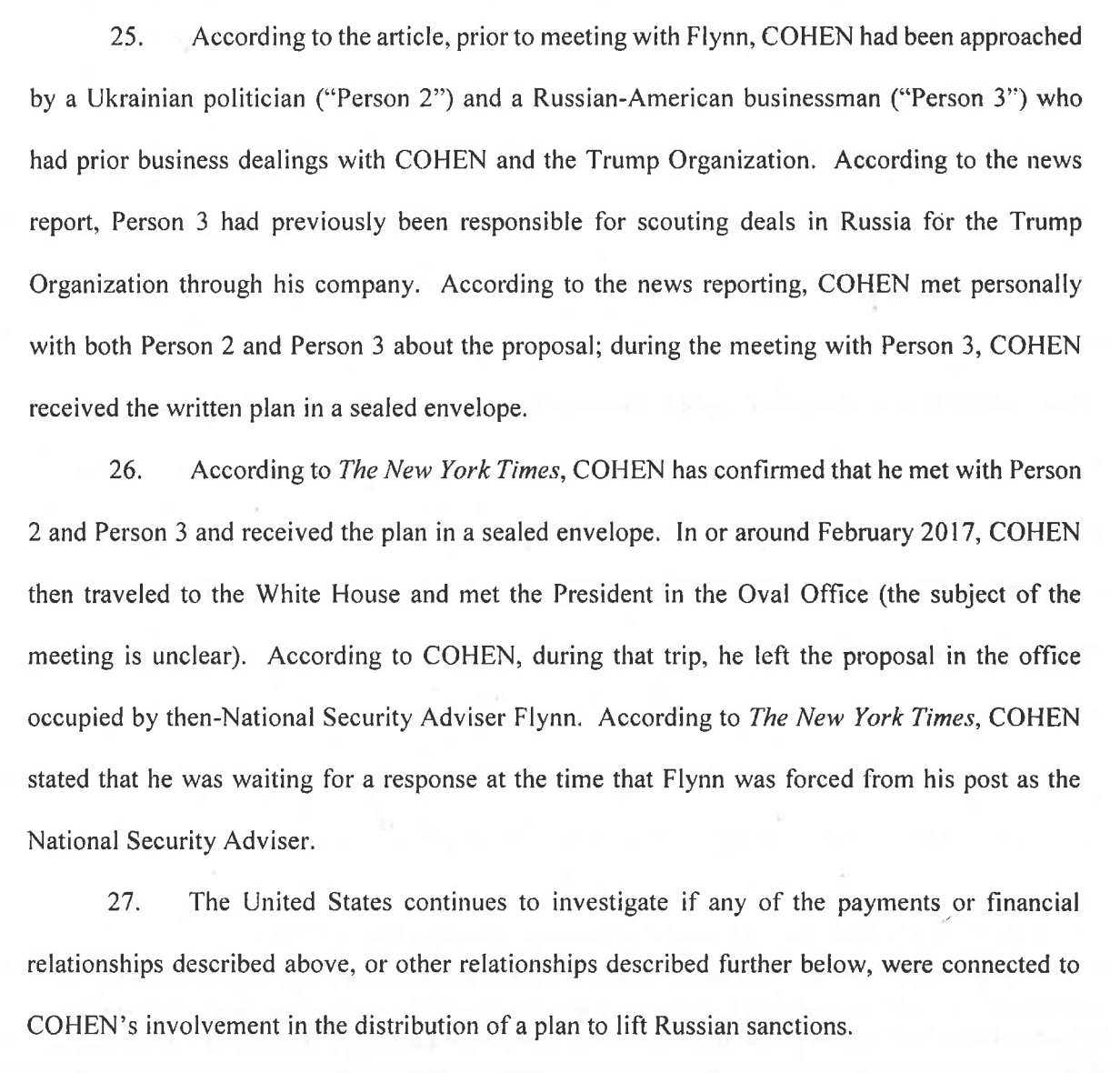

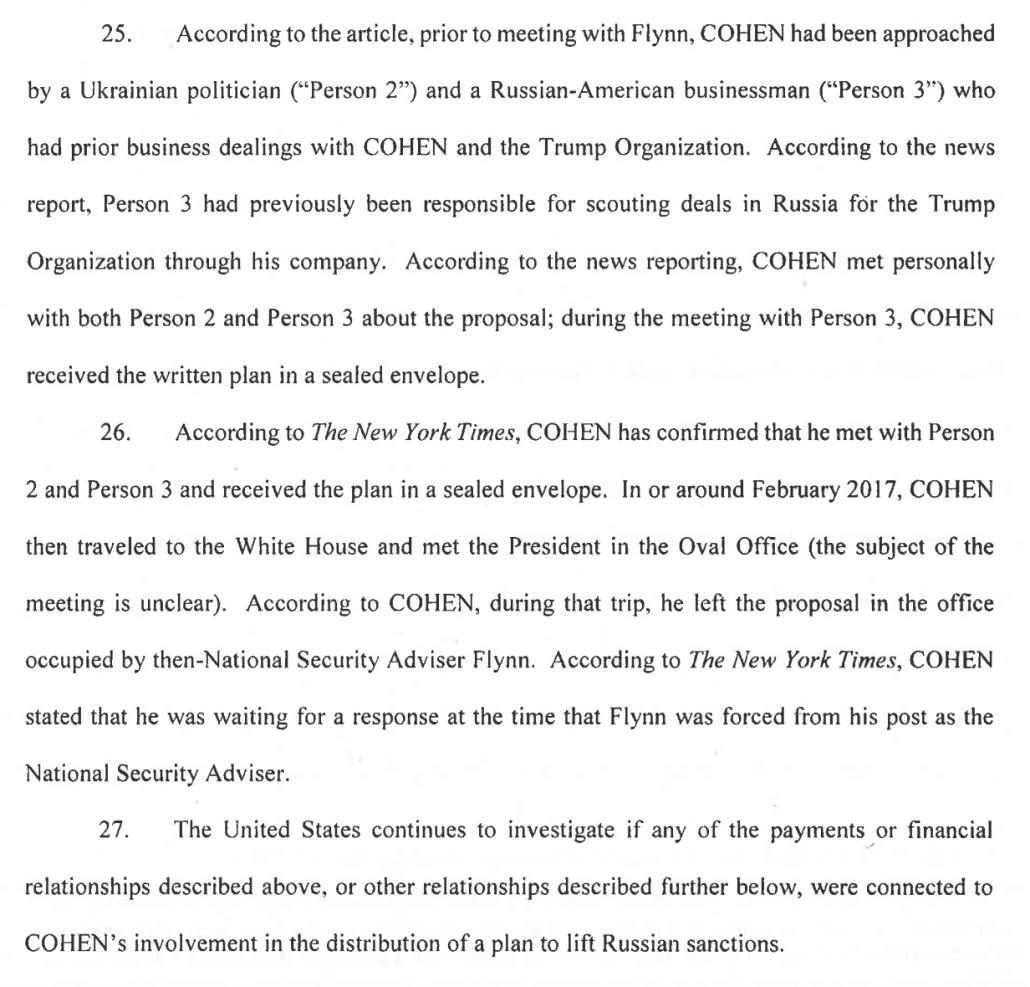

The reason those payments were such a concern is that, as the NYT itself reported on February 19, 2017, Andrii Artemenko (Person 2) and Felix Sater (Person 3) had used Cohen to pitch a “peace deal” for Ukraine to Mike Flynn.

The warrant affidavit really downplayed the substance of the NYT story, which described Artemenko claiming that the “peace plan” “he had received encouragement for his plans from top aides to Mr. Putin.” In the story, Cohen excused chasing a plan with support from Russia based on Artemenko’s claim to have proof of corruption implicating then Ukrainian President, Petro Poroshenko.

After speaking with Mr. Sater and Mr. Artemenko in person, Mr. Cohen said he would deliver the plan to the White House.

Mr. Cohen said he did not know who in the Russian government had offered encouragement on it, as Mr. Artemenko claims, but he understood there was a promise of proof of corruption by the Ukrainian president.

“Fraud is never good, right?” Mr. Cohen said.

Cohen’s claim that, “Fraud is never good,” did not make the warrant affidavit that would set off an investigation that would lead to the conviction of Donald Trump on 34 counts of fraud.

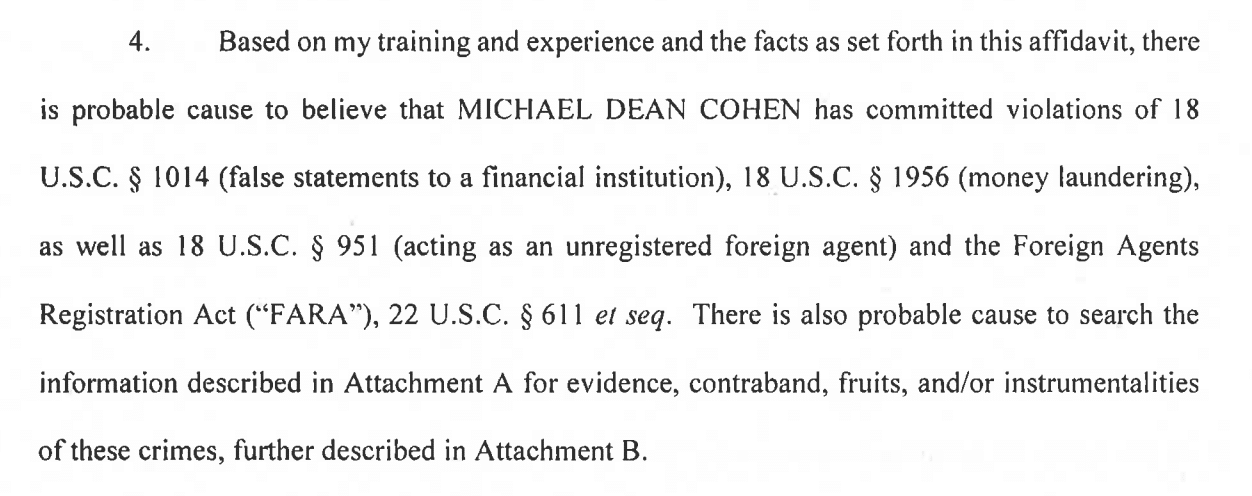

The payments from Columbus Nova — along with payments from Korea Airspace Industries, Kazkommertsbank, and Novartis — would undoubtedly have resulted in SARs in any case. But given the report on the “peace deal,” it substantiated probable cause to suspect that Cohen was acting as an agent of a foreign power and/or violating FARA, which statutes were two of the four crimes the warrant authorized the FBI to investigate.

But false statements to a financial institution were also in there, in part, lying to First Republic about using the Essential Consultants account to pay off porn stars and accept big payments from foreign companies.

Michael Cohen, and so, Donald Trump, was not investigated simply because he had ties to Donald Trump. Claiming he was ignores the public record, including legal and reporting work done by the NYT. It ignores Cohen’s actions, including boneheadedly stupid moves he made as he tried to profit from his proximity to Trump.

He was investigated because he lied to his bank and then, even as he was making public comments about entertaining a “peace deal” with Russian involvement, used the bank account associated with the hush payment to accept big payments from a prominent Russian oligarch.

Importantly, this predication — a SAR implicating a politically exposed person about big payments from a foreign company — is far more than what predicated the investigation, and now six years of non-stop attention from the GOP, into Hunter Biden. That investigation started from a SAR about sex workers, from which an IRS agent fished out Hunter Biden’s name and then spent seven months digging before using Burisma to predicate a grand jury investigation.

If mouthpieces for Trump’s DOJ have a problem with this investigation, then they should be speaking out even more loudly about the investigation into Hunter Biden in which Bill Barr personally tampered.

Update: Corrected an error where I transposed the number of fraud counts Trump was convicted on. It’s hard to keep count!

Update: Isgur is out with an op-ed that scolds Hunter Biden he should plead guilty, without noting that to appeal the motion to dismiss based on the reneged plea deal, he can’t do that. Isgur also doesn’t mention that the gun shop doctored the form.