‘Look, You Can Live on Minimum Wage!’ Say Modern Slavers

[Sample budget via McDonald’s and VISA]

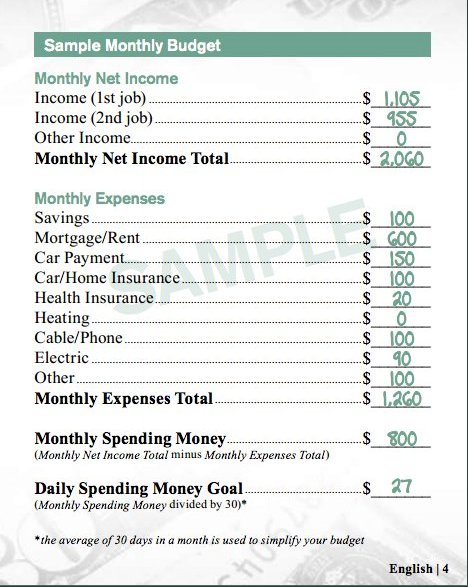

After looking it over, here’s my assessment: A couple corporations need to do drug testing among white-collar staff. Somebody had to be be out of their gourd to think this was accurate, let alone an effective marketing tool to promote their businesses.

As many folks have pointed out, an immediate glaring error on this ‘budget cheat sheet’ is the lack of heating/cooling expenses. Sure, some apartment complexes included HVAC in the rent they charge, but this can’t be assumed as a norm.

Every line item included is grossly flawed. I’ll look at three points:

1) First job’s NET salary of $1105 based on an estimated 21% income tax equals ~$1400 gross salary. Based on current federal minimum wage of $7.25 per hour, that’s ~193 hours worked in a month, or ~44.6 hours a week.

This is NOT a part-time job. Most fast food jobs are deliberately limited to under 32 hours a week to avoid paying unemployment taxes or other benefits.

2) Second job’s NET salary of $955 — HAHAHAHAHAHAH Right. That’s another ~167 hours of labor per month at current federal minimum wage and 21% income tax rate.

To make this sample budget work, either two people MUST live together, MUST work a combined ~83 hours a week at current federal minimum wage. Or one person must do all this and simply have no time to do anything beyond eat/sleep/bathe/maybe laundry.

If two people lived together to make this budget work, they MUST share a tiny/cheap/ratty car, or hope like hell there’s public transportation which costs less than $150 a month to get to/from ~83 hours of work, grocery store, school, so on.

The rest of the assumptions in this budget are just plain trash. Like health insurance for two people versus one. Or savings of $100 which is really half that, spread between two people, as is the discretionary daily spending.

Some trollish account said, “But nobody stays at minimum wage forever! They get pay increases!” Sure…now person working First Job only has to work 43 hours a week instead of ~44.6. The average wage at McDonald’s is $8.25 — but does that include assistant managers and shift managers? Does this include people who’ve worked at McD’s for years? Let’s be real: most fast food workers are closer to the federal minimum wage.

Perhaps with pay increase a person working BOTH jobs only has to work ~80 hours a week instead of ~83. Give me a fucking break.

3) Transportation and insurance combined = $250 — HAHAHAHAHAHAH Right, again. I checked Progressive’s website calculator for insurance on a vehicle only, assuming a 2007 4-door Honda Civic, personal use, unmarried single male driver age 18-24 living alone, who lived in the same rented home for 1-3 years, had driven for more than 3 years, had insurance for 1-3 years, assuming a 20-year old male student living in Lansing, Michigan. Car insurance alone was $219 per month AND +$400 was required upfront before coverage began.

Maybe bundling renter’s insurance would help but the cost McDonald’s and VISA used in their example budget for insurance and a used car loan is simply unmoored from reality.

And perhaps insurance is cheaper in other parts of the country, but I will bet good money some other line item in that budget increases. Like the cost of an annual automobile license (higher in FL than MI) or a mandatory vehicle emissions test (required in CA but not MI).

Roughly 50% of Americans can’t get their hands on $400 cash for an emergency. Imagine if your insurer dropped you and you’re a fast food worker living to this prospective budget. That’s where VISA comes in with an opportunity to finance your emergency, compounding the stranglehold minimum wage has on your life.

God help you if you’re trying to put yourself through college without scholarships or family assistance. Even the imaginary example student attending Lansing Community College will pay more than $65,500 for four years. How long will it take to get through a four-year degree if one works ~83 hours a week? How long will it take to pay off school loans if one manages to break out of fast food service work after graduation — let’s say they double or triple their wages to $14.50 or $21.75 hour? This prospective student faces somewhere between 12 and 15 years of payments ranging from $950 to $1050 per month, and payments may begin as early as NOW while attending school at $650 per month.

You will be in debt for much of your adult life. There will be no extra money for anything.

Maybe the rare avocado toast, if you can find one marked down in the Damaged bin or live someplace warm where fallen avocados can be found for free. And maybe if you can afford bread this week.

“But millennials buying pricey iPhones!” some out-of-touch jackass might say. Let’s say you’re a fast food worker who might have to change housing at any time because rent has increased dramatically in your city. Even my example dude in innocuous Lansing faces a +7% increase in rent each year though his wages have been stagnant. Your entire life — telephone, computer, internet access, records, more — resides in a single, portable device. Of course you’ll pay more for a phone which hails a tow truck when your ratty little car breaks down, or finds you a quick cash gig (or a plasma blood bank) to pay for repairs. That phone is your lifeline, the lifesaver you can count on unlike white-collar jerk-offs who have no clue what you’re going through to survive.

And God help you if you get sick or injured. You can’t count on your elected officials to make sure you’ll be healthy enough to show up to work those ~83 hours a week.

Indentured servitude, without a contract, that’s what this budget reflects. Product marketing by modern slavers.

And they can’t understand why millennials are killing so many things like fast food businesses. They simply can’t afford them.